Why Cash Beats Profit (Cash is the King)

Cash-Flow-First Guide — with worked examples (Alibaba & Netflix) and a reusable framework applied for my current holdings.

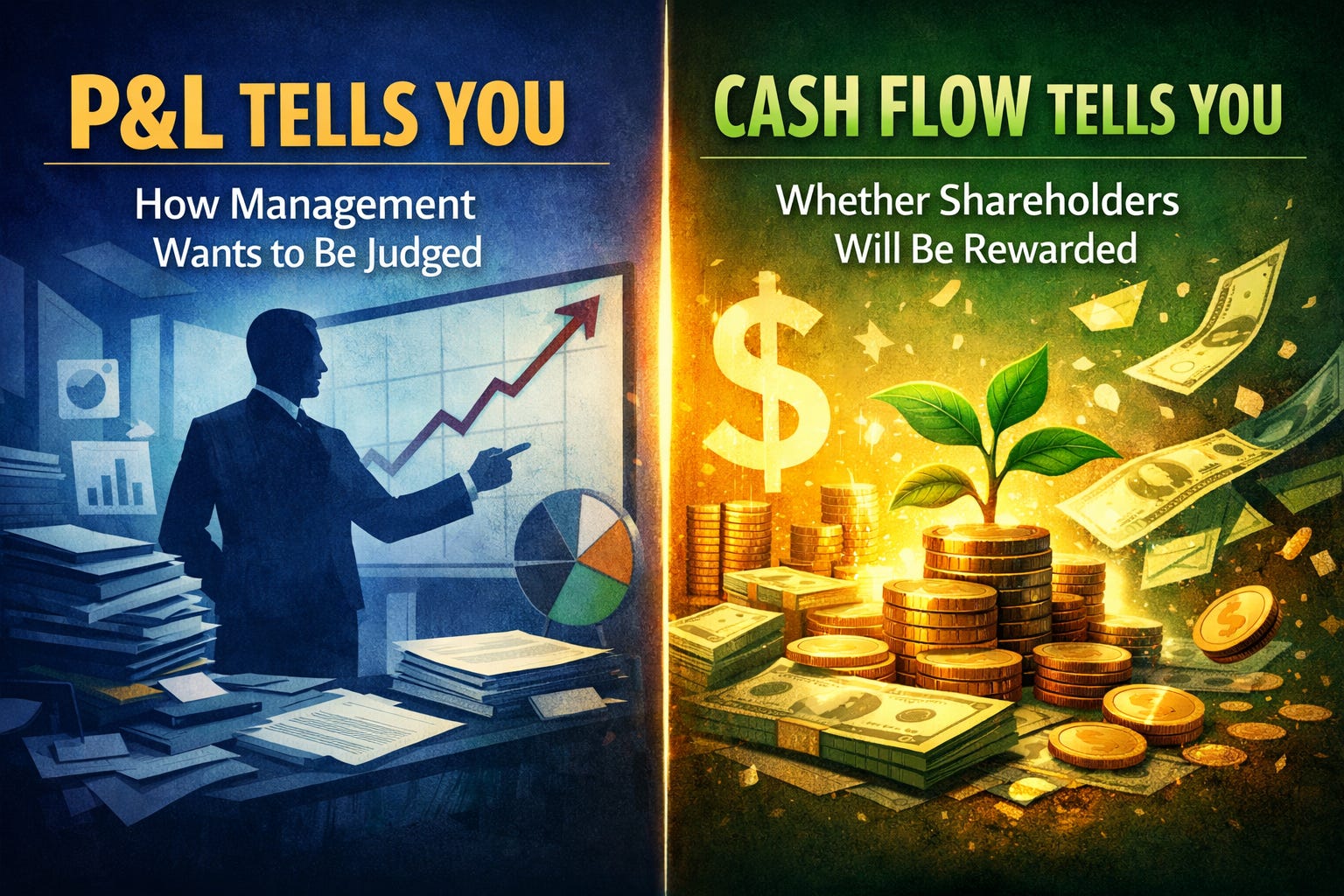

Investors talk about revenue growth, margins, and EPS. But the only thing that actually pays investors — dividends, buybacks, debt repayment, or reinvestment that creates value — is cash. Prof. Damodaran’s central teaching is simple: value is the present value of expected cash flows. This post explains why OCF and FCF matter more than the P&L, then I have applied Prof. Damodaran’s teachings to apply a cash-flow valuation framework to Alibaba and Netflix — and shows why a cash-first analysis supports my strategies towards Alibaba and Netflix in my portfolio.

1. The Core Argument — Why FCF (and OCF) Matter More Than the P&L

Accounting ≠ Economics. Net income is shaped by accruals, non-cash charges, amortization and accounting choices. FCF is the actual cash available to the firm and shareholders.

Harder to fake. Management can smooth earnings; it’s far harder to fake cash collected from customers or cash paid out. Big and persistent divergence between net income and OCF is a red flag.

Capital allocation is visible in cash. True discipline shows up when OCF funds maintenance CapEx, required reinvestment, and still leaves cash for debt paydown, dividends, or buybacks.

Reinvestment must earn more than the cost of capital. Weak FCF alone is not necessarily bad — it may reflect heavy reinvestment. But if incremental ROIC ≤ WACC, reinvestment destroys value. Damodaran insists on this test.

value lies in normalized economic cash flows. Use FCFF/FCFE, normalize reinvestment, estimate a realistic cost of capital (WACC), and test whether reinvested capital earns excess returns. Stories matter only insofar as they can be translated into credible, testable cash-flow numbers.

2. A Simple, Publishable Framework

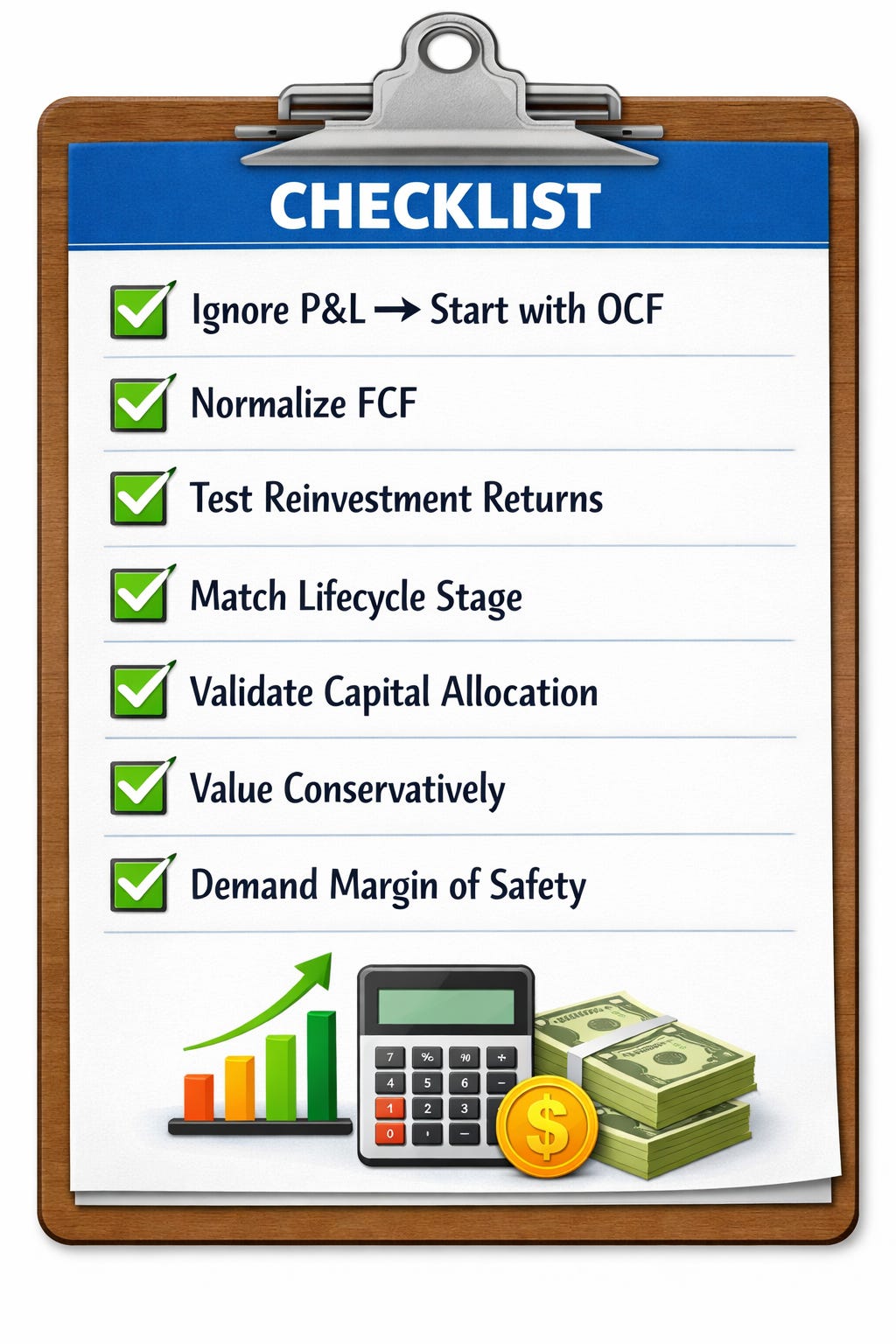

The Cash-First Checklist

Collect (annual preferred; 3–5 years): OCF, CapEx, FCF (OCF − CapEx), AR / Inventory / AP, Net debt, shares outstanding, management guidance.

OCF health: Trend OCF. Calculate cash conversion = OCF / Net Income. Watch for large, persistent gaps.

Normalize FCF: Separate maintenance CapEx from growth CapEx. Compute Economic FCF = OCF − maintenance CapEx − required reinvestment.

Reinvestment quality: Estimate incremental ROIC (or proxy). Compare to WACC. If ROIC > WACC, reinvest. If ROIC ≤ WACC, return cash.

Lifecycle alignment: Classify the company: growth / scaling / mature / harvest. Cash behavior must match stage.

Capital allocation test: Are buybacks/dividends funded by FCF (good) or by new debt/issuances (warning)?

Valuation mechanics: Project normalized FCF (5–10 years), discount at WACC, choose a terminal value (conservative multiple or Gordon growth), do sensitivity analysis.

Decision rule: Hold if intrinsic value > market price by margin of safety and FCF/reinvestment quality is sound. Trim/Exit if FCF trends down or reinvestment lacks ROIC proof. Add if FCF improvement is visible and durable.

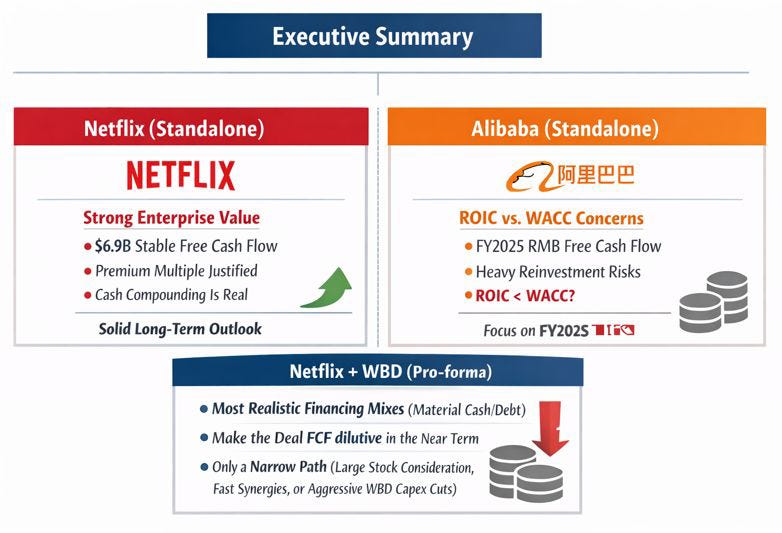

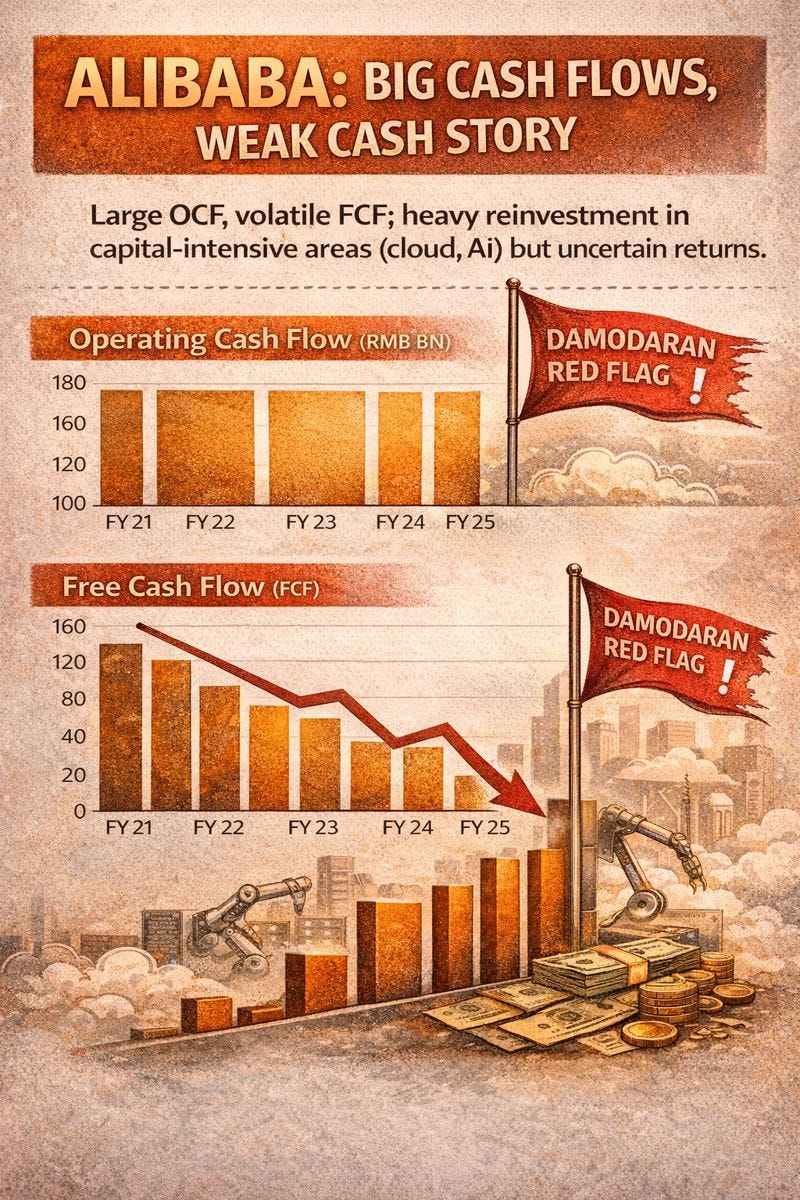

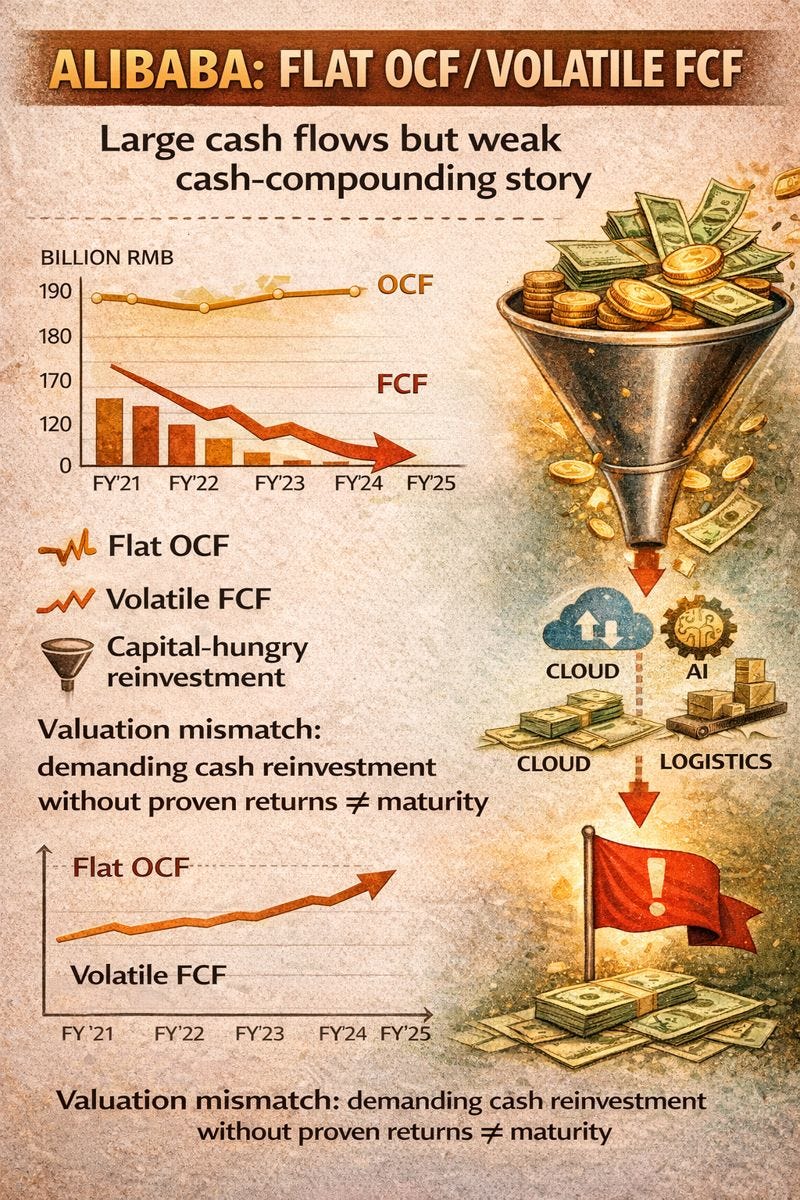

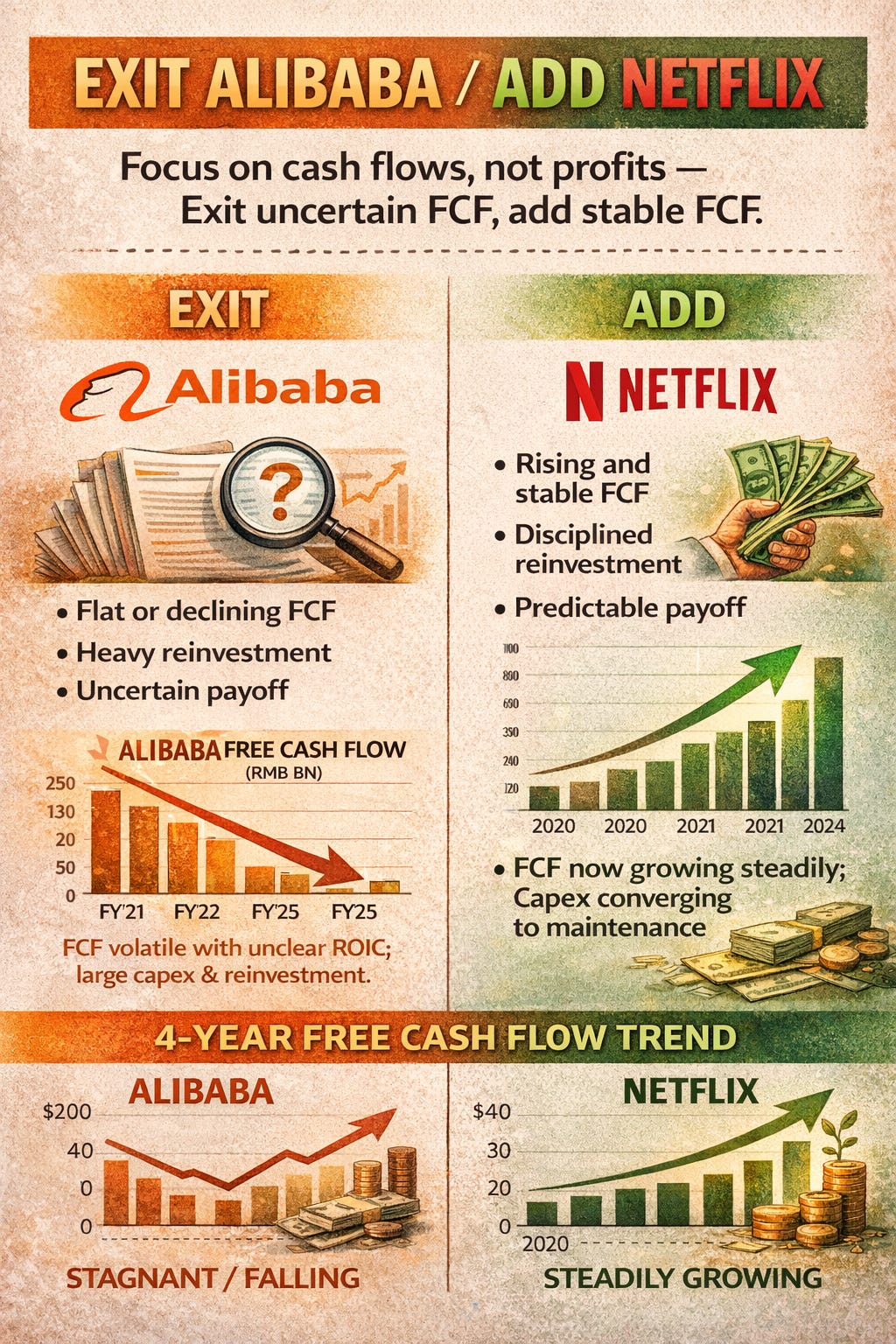

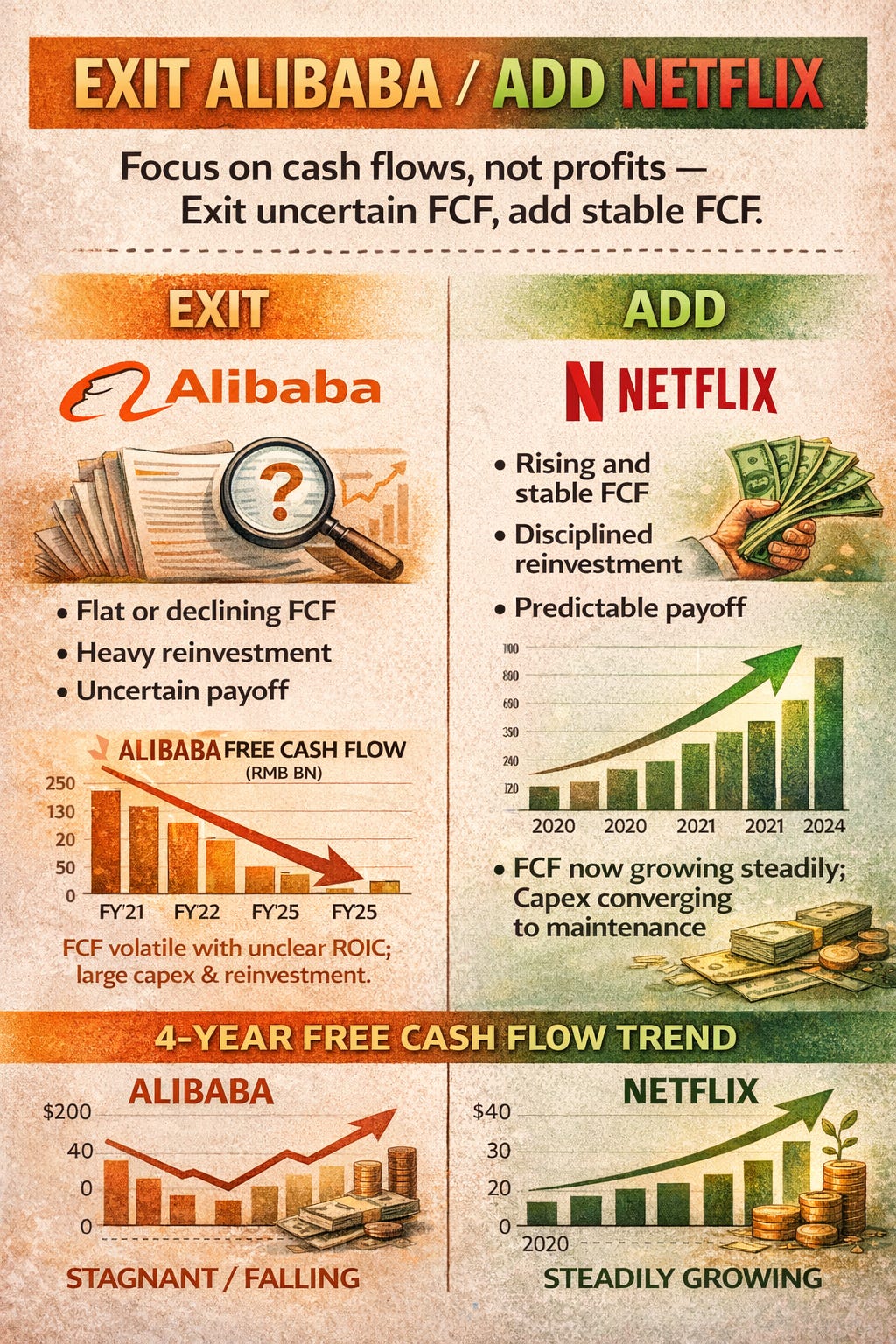

3. Worked Example — Alibaba (Why I’m Exiting)

Alibaba has large nominal cash flows but a weak cash-compounding story: OCF is big but flat, FCF is volatile, and management is redeploying cash into capital-intensive areas (cloud, AI, logistics) without clear public proof those investments will earn excess returns. That mismatch — a company claiming maturity but behaving like a capital-hungry growth firm — is a Damodaran red flag.

Cash-centric observations (summary)

OCF: Large in absolute terms but not compounding consistently.

CapEx & reinvestment: Increasing; management is plowing cash into cloud/AI and logistics.

FCF: Volatile and compressed when reinvestment spikes. FYs with large reinvestment see FCF fall despite steady OCF.

Capital allocation: Focus on reinvestment rather than consistent, shareholder-focused returns (buybacks/dividends) funded by FCF.

ROIC visibility: Public filings do not clearly demonstrate that incremental reinvestment will earn ROIC > WACC.

If Alibaba’s incremental ROIC on cloud/AI > WACC, reinvestment is justified. But without evidence, heavy reinvestment without FCF compounding looks like value destruction or at best increased risk — therefore, trim or exit is the prudent cash-first position.

Practical decision

Exit or reduce position unless the company provides clear, measurable ROIC evidence for its reinvestments or FCF starts steadily compounding again.

4. Worked Example — Netflix (Why I’m Adding)

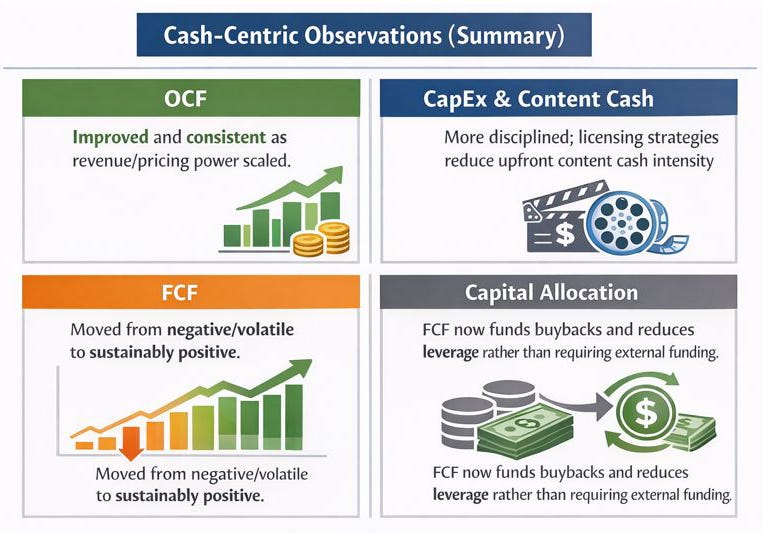

Netflix successfully transitioned from heavy cash-burn (high upfront content spend) to a disciplined, cash-generating model (licensing mixes + pricing + scale). That shift turned volatile/negative FCF into sustained positive FCF, making Netflix a cash compounder — the type of business Damodaran values highly.

Cash-centric observations (summary)

OCF: Improved and consistent as revenue/pricing power scaled.

CapEx & content cash: More disciplined; licensing strategies reduce upfront content cash intensity.

FCF: Moved from negative/volatile to sustainably positive.

Capital allocation: FCF now funds buybacks and reduces leverage rather than requiring external funding.

Netflix’s past reinvestments appear to be producing returns (ROIC > WACC), and now the company harvests cash. This fits Damodaran’s model: fund the growth stage, then harvest with disciplined allocation.

Practical decision

Add Netflix as a high-quality cash compounder — justified even at a premium if you believe FCF is stable and reinvestment needs have normalized.

5. Valuation Outline (FCF-Only)

Start with normalized FCF (use 3-5 year median, adjust for known structural shifts).

Project explicit FCF for 5–10 years using conservative growth assumptions (use scenario bands).

Estimate WACC (industry beta proxy, capital structure, risk-free rate, credit spread).

Discount projected FCF to present value; compute terminal value (Gordon growth with conservative g or 10–20× FCF terminal multiple, whichever is more conservative).

Do sensitivity analysis on: long-term FCF growth, WACC, and maintenance CapEx.

Compare intrinsic value per share to market price. Apply margin of safety.

(Note: For platform companies that have shifted to harvest phase, emphasize terminal FCF and lower required reinvestment.)

Cash conversion (OCF / Net Income): >1.0 = strong; <0.7 = investigate.

FCF yield (FCF / Market cap): >5% attractive; 3–5% reasonable for high quality; <3% expensive unless growth is nearly certain.

Net debt / OCF: >4x = watch leverage.

CapEx signal: CapEx >> depreciation for multiple years = heavy reinvestment; probe ROIC.

Dividend/buybacks funded by debt: red flag.

6. Key Takeaways

Start with cash, not the income statement.

Weak FCF is a question, not a verdict — always pair with ROIC vs WACC.

Lifecycle matters: growth firms can have negative FCF; mature firms should compound FCF.

Netflix = cash compounder now; Alibaba = capital-hungry with unclear ROIC. Your allocation decision — exit Alibaba, add Netflix — matches a Damodaran-compatible, cash-first discipline.

Do the math: always build simple FCF scenarios and run conservative sensitivity tests before changing position size.

How to Use the One-page Checklist

This is your pre-buy / pre-sell gatekeeper

Use it before every position change

If a stock fails two or more check items → do not add

This is exactly why:

Alibaba failed (uncertain ROIC + volatile FCF)

Netflix passed (disciplined reinvestment + real FCF)

Let me re do the exercise with WBD (Warner Bros) deal going on

What I changed and why

Netflix: updated FY2024 OCF ≈ $7.361B and FCF ≈ $6.922B (source: company Q4 release / 2024 annuals). I used weighted-average diluted shares ≈ 431m for per-share math.

Alibaba: updated FY2025 OCF ≈ RMB 163.509B and FCF ≈ RMB 73.87B from Alibaba’s FY2025 results.

WBD: used FY2024 OCF ≈ $5.4B, FCF ≈ $4.4B, net debt ≈ $30B (reported).

Pro-forma Netflix + WBD: used the same scenarios we discussed (low vs high CapEx for WBD) and sensitivity to new debt issuance and interest cost. I computed FCF after interest and ran a two-stage DCF (5-year explicit + Gordon) using conservative WACC inputs.

Quick interpretation of the outputs

Netflix (standalone) — DCF shows a strong enterprise value driven by stable FCF (~$6.9B). On conservative WACC and growth assumptions the company justifies a premium multiple because cash compounding is real.

Alibaba (standalone) — The RMB DCF shows Alibaba’s enterprise value in local currency terms based on FY2025 FCF; the key investor question remains whether Alibaba’s heavy reinvestment will earn ROIC > WACC — this is the reason to consider exiting or trimming.

Netflix + WBD (pro-forma) — Most realistic financing mixes (material cash/debt) make the deal FCF-dilutive in the near term. Only a narrow path (large stock consideration, fast synergies, or aggressive WBD capex cuts) preserves Netflix’s per-share FCF profile.