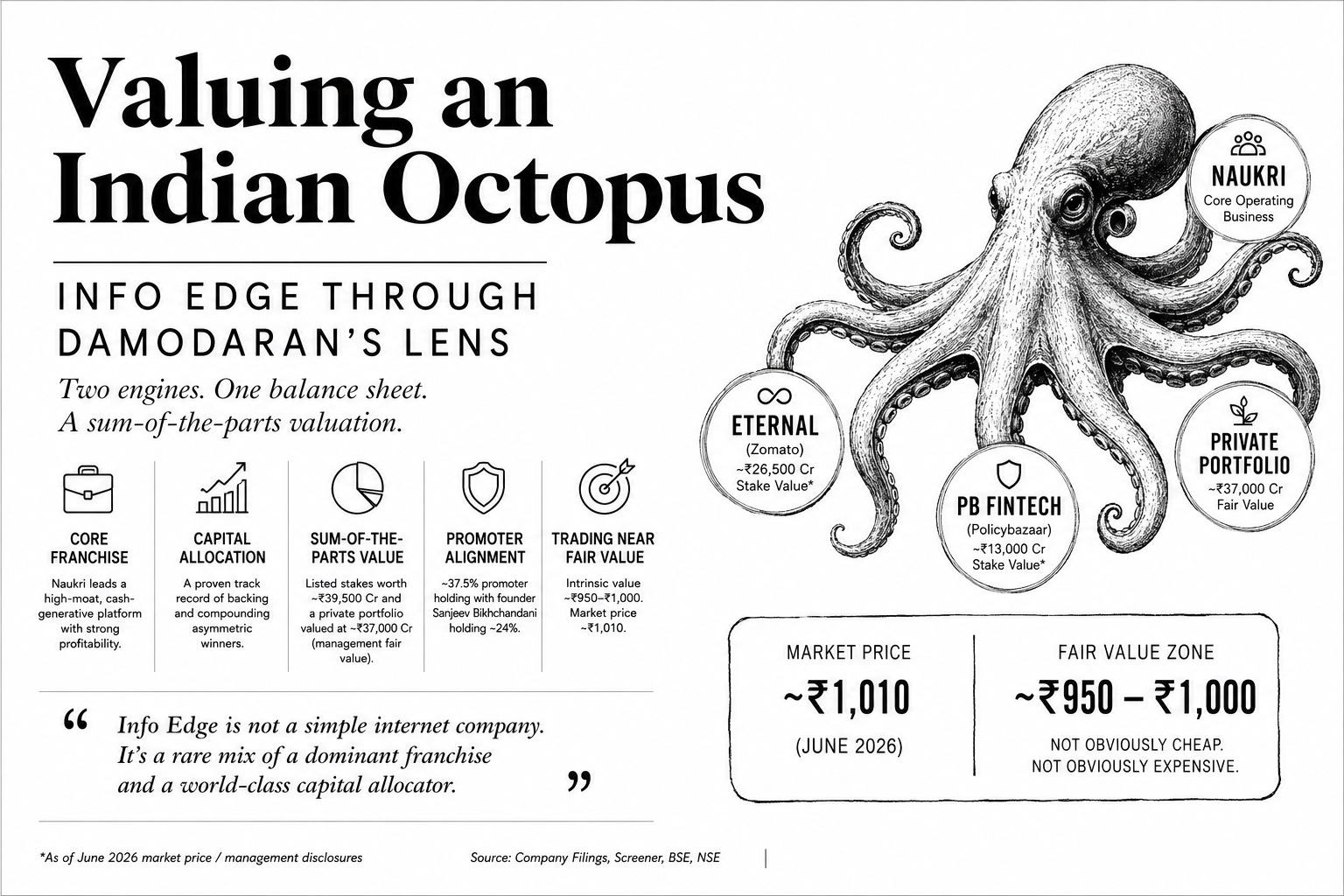

Valuing an Indian Octopus: Info Edge Through Damodaran’s Lens

Two engines. One balance sheet. A sum-of-the-parts valuation.

DISCLAIMER: This article is part of my personal learning journey and is meant purely for educational and informational purposes. I have drawn insights from Prof. Aswath Damodaran’s publicly available teachings and financial information available in the public domain.

While preparing this write-up, I referred to platforms such as Screener and AI-based study tools to better understand the concepts and validate publicly available data such as company filings and information available for investors from the company domain. The interpretations and conclusions shared here are entirely my own, and any errors or misunderstandings are solely my responsibility.

This is not investment advice or a recommendation to buy, sell, or hold any securities. I encourage readers to do their own research and consult a SEBI-registered investment advisor before making any investment decisions.

Key Takeaways

Info Edge is best understood as two businesses under one roof: a dominant internet classifieds franchise and a highly successful venture investment engine.

Traditional valuation multiples can be misleading because a significant portion of the company’s value comes from listed and unlisted investments.

A sum-of-the-parts framework, inspired by Aswath Damodaran’s valuation approach, is the most appropriate way to analyze the company.

The core operating business appears to be a high-quality, cash-generative franchise with strong margins and durable competitive advantages.

At current prices, the stock appears to be trading around fair value rather than at a significant discount.

Future returns will likely depend on both the continued strength of the Naukri ecosystem and the success of the next generation of startup investments.

When I look at Info Edge, I do not see a normal listed company. I see two businesses stitched together: a dominant, cash-generating internet classifieds franchise led by Naukri, and a venture-style investment engine that has produced extraordinary value through stakes such as Eternal and PB Fintech.

That is exactly why I think Info Edge is one of the best Indian case studies for applying Professor Aswath Damodaran's framework. Damodaran has repeatedly argued that cash, cross-holdings, and other non-operating assets should be valued separately from the operating business. In his discussions on holding companies and cross-holdings, he notes that the "sum of the parts" can often be greater than the whole when these assets are not properly accounted for. For a company like Info Edge, where listed and unlisted investments contribute materially to shareholder value, a sum-of-the-parts approach is not optional—it is essential.1

In Info Edge’s case, that distinction is not academic. As of June 2026, the company itself had a market capitalization of roughly ₹65,000 crore, while a substantial part of its value sat in listed investments and a startup portfolio that management valued at nearly ₹37,000 crore.

So the right question is not, “Is Naukri expensive on earnings?”

The right question is:

How much am I paying for the core franchise after adjusting for Eternal, PB Fintech, and the next cohort of private investments?

Why Info Edge Is a Perfect case study for understanding Prof. Damodaran’s lens

Damodaran’s valuation philosophy begins with a story and then forces the numbers to be consistent with that story.

My story for Info Edge is simple.

The first engine is a high-quality operating business with a durable moat in recruitment classifieds, strong operating leverage, and real free-cash-flow discipline.

The second engine is a capital allocator with a demonstrated ability to identify, back, and hold asymmetric winners for long periods.

That combination makes Info Edge unusual.

Many companies are either operating businesses or investment vehicles.

Info Edge is both.

Naukri remains the core cash machine, but the market’s view of the company is also shaped by what happened with Zomato—now Eternal—and with Policybazaar through PB Fintech.

This also explains why plain P/E ratios can mislead. Reported earnings often include large amounts of investment-related income and mark-to-market effects, creating accounting noise that distorts headline valuation multiples.

The Operating Story I Am Telling Myself

When I strip away the investment book, I am left with a business that is significantly better than a typical Indian internet company.

FY25 standalone revenue was approximately ₹2,654 crore, operating profit was around ₹973 crore, and the starting EBIT margin in my model was roughly 36.7%.

That is not what a fragile, capital-hungry internet business looks like.

It looks like a platform business with real pricing power and low incremental capital intensity.

Info Edge’s own disclosures increasingly describe Naukri as evolving from a traditional job-search platform into a broader talent ecosystem. That matters because deeper workflow relevance typically strengthens both customer stickiness and monetization potential.

The cash-flow quality is equally important.

Free-cash-flow conversion remains strong, and cash generation has consistently supported both internal reinvestment and external venture investments.

That cash discipline sits at the center of my thesis.

In a Damodaran framework, earnings are only useful if they can be converted into cash and distributed or reinvested intelligently.

Info Edge passes that test far better than many businesses trading on technology narratives.

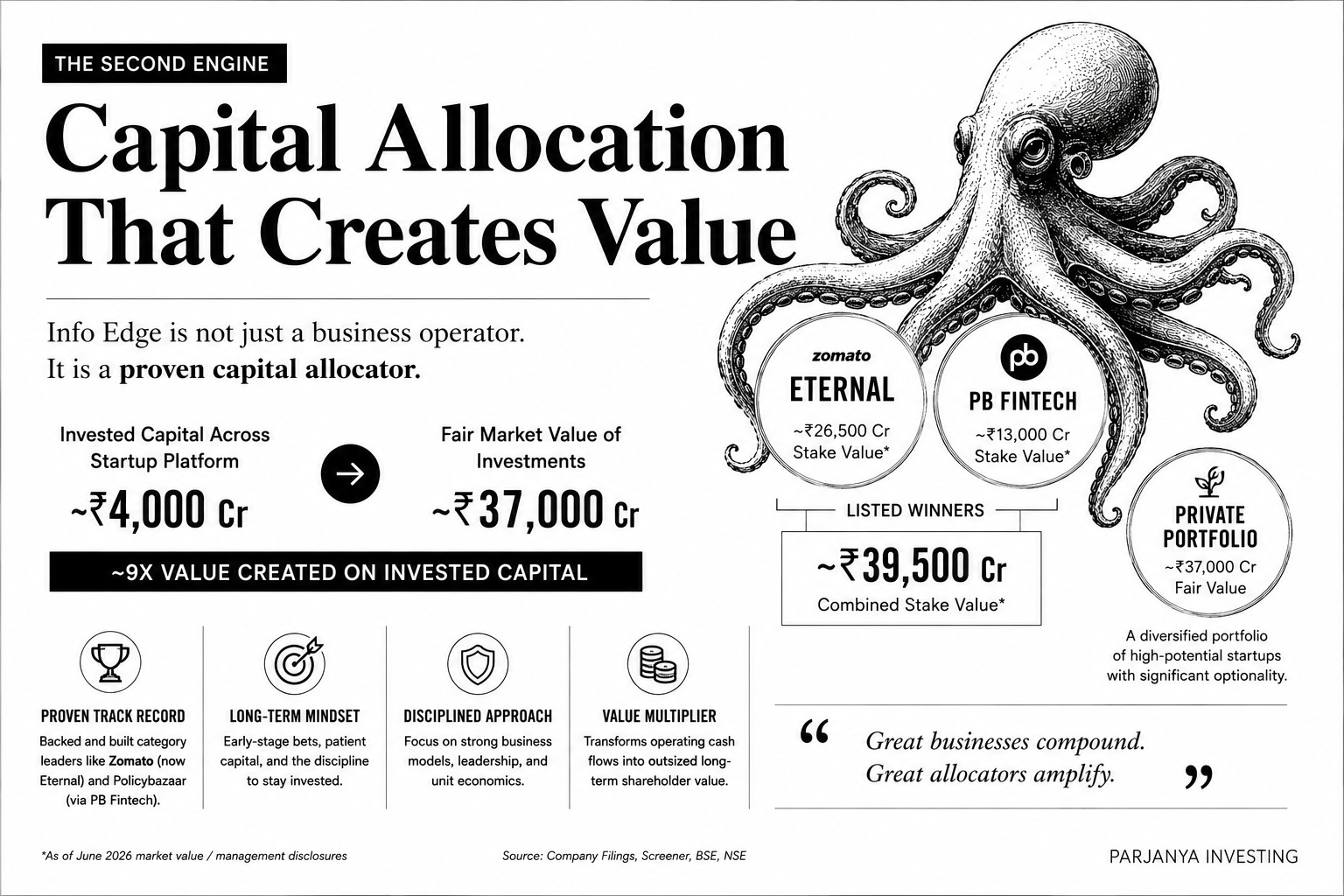

The Second Engine: Capital Allocation

The other half of the story is where Info Edge becomes truly distinctive.

Management disclosed that total invested capital across its startup platform stood at roughly ₹4,000 crore, while the fair market value of those investments approached ₹37,000 crore.

Those are extraordinary numbers.

More importantly, they fundamentally change how I think about the balance sheet.

This is not idle treasury cash.

This is a portfolio that has already produced two listed winners and still carries meaningful optionality from the rest of the investment book.

The listed winners are the easiest to value.

Using June 2026 market values, Info Edge’s stakes in Eternal and PB Fintech together were worth approximately ₹39,500 crore.

That single number explains why this company must be valued in pieces.

If the market capitalization is roughly ₹65,000 crore and the two listed holdings alone are worth nearly ₹40,000 crore, then the market is implicitly assigning the remaining value to the core operating franchises plus the unlisted portfolio.

How I Split the Business

Damodaran’s treatment of cash and cross-holdings provides the right starting point.

First, value the parent company’s operating assets.

Second, value the holdings separately.

Third, decide whether those holdings deserve to be added at full value or at a discount because of taxes, opacity, or governance considerations.

For Info Edge, I split the company into three buckets:

The core operating business: Naukri, 99acres, Jeevansathi, Shiksha, and other controlled operating assets.

The listed investment book: Eternal and PB Fintech.

The private portfolio: the broader startup portfolio, valued through probability-weighted assumptions and appropriate haircuts.

Once I do that, the valuation becomes much clearer.

I no longer have to force one multiple to explain two fundamentally different economic engines.

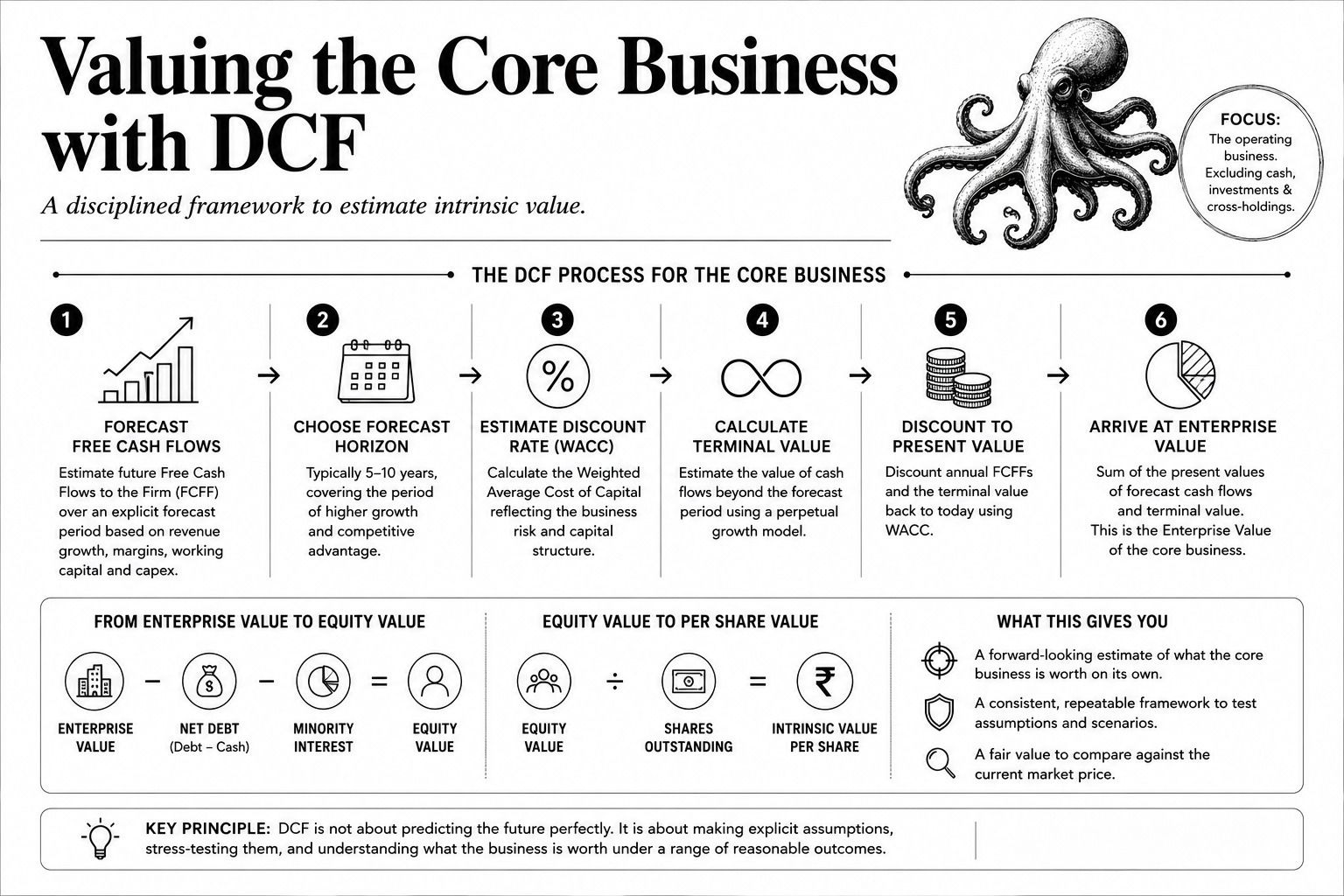

My Core-Business DCF

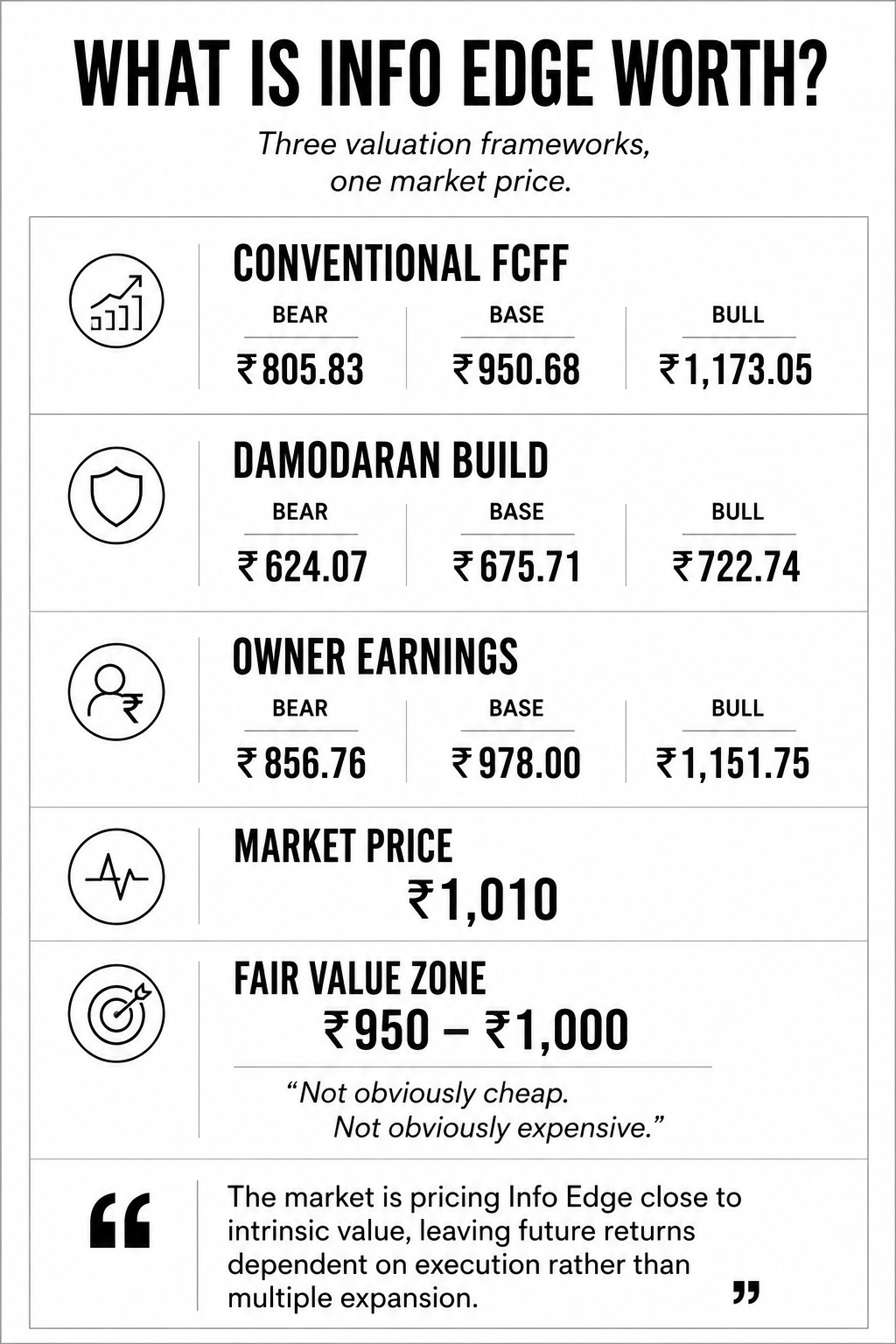

I built three versions of the core-business valuation.

The first was a conventional FCFF model.

The second was a stricter Damodaran-style build with a higher cost of capital and explicit return-on-capital fade.

The third was an owner-earnings model that treats Info Edge more like a high-ROIC platform business with low maintenance reinvestment requirements.

The conventional FCFF model produced an intrinsic value range of:

₹805.83 to ₹1,173.05 based on Bear to Bull scenario

The stricter Damodaran build produced:

₹624.07-₹675.71-₹722.74(Bear-Base-Bull)

The owner-earnings model produced:

Bear₹856.76, Base₹978.00, Bull₹1,150.75

I do not treat any one of these as the truth.

I treat them as a range generated by different but intellectually honest stories about the business.

That is very much in the spirit of Damodaran: valuation is a disciplined conversation between narrative and numbers, not a hunt for a fake precision point estimate.

What the Three Models Are Really Saying

Taken together, these models say something simple.

Info Edge is not obviously cheap.

But it is also not wildly expensive if I believe the core operating franchise deserves a premium for moat, cash conversion, and capital allocation quality.

The overlap zone between my more realistic base cases falls roughly between ₹950 and ₹1,000 per share.

That sits remarkably close to where the market currently values the stock.

My conclusion is not that the stock is a bargain.

My conclusion is that the stock is trading around intrinsic value, with modest upside or downside depending on how optimistic I choose to be about the operating business and how much of the private investment book I am willing to recognize.

Why the Private Portfolio Cannot Be Ignored

A lot of investors stop after marking Eternal and PB Fintech.

I think that is incomplete.

It is easy to value listed stakes and pretend the rest of the startup book is noise.

Management’s disclosures suggest otherwise.

At the same time, I do not want to value the private portfolio lazily.

For early-stage companies, the right framework resembles venture-capital valuation rather than traditional DCF analysis.

Estimate a plausible exit value.

Assign a probability of success.

Adjust for dilution.

Discount back at a sufficiently high required return.

That is why, in my own sum-of-the-parts framework, I do not add the startup portfolio at full value by default.

I use scenario-based weights and meaningful haircuts rather than assuming every fair-value mark will eventually translate into realized gains.

Promoter Skin, Moat, and Cash Discipline

My three favourite lenses for evaluating businesses are:

Moat

Promoter skin in the game

Free-cash-flow discipline

Info Edge scores well on all three.

Promoter ownership remains meaningful at approximately 37.5%, with founder Sanjeev Bikhchandani individually holding about 24% of the company. This level of ownership creates strong alignment between management and minority shareholders, particularly in a business where long-term capital allocation is a major driver of value creation.

When founders continue to own a meaningful portion of the business after decades of operation, I generally have greater confidence that capital allocation decisions are being made with a long-term mindset.

On moat, the easiest evidence is visible in the economics of the core business.

A business generating EBIT margins north of 35%, producing strong free cash flow, and maintaining leadership in a category for years is rarely doing so by accident.

Those economics are often downstream manifestations of:

Brand strength

Network effects

Embedded workflows

Customer inertia

Rational competition

Naukri benefits from several of these simultaneously.

Employers want access to the largest candidate pool.

Candidates want access to the largest number of recruiters.

That creates a reinforcing flywheel that becomes increasingly difficult for competitors to replicate.

On cash-flow discipline, the story becomes even stronger.

The company has remained largely debt free while continuing to:

Fund organic growth

Invest in adjacent businesses

Build a venture portfolio

Maintain balance-sheet flexibility

That combination is surprisingly rare.

Many firms with venture portfolios lack a strong operating engine.

Many cash-generative firms struggle to identify high-return external investments.

Info Edge has demonstrated an ability to do both.

The Buy-Below Levels I Would Use

Because the stock appears to be trading around fair value, I think price discipline matters more than enthusiasm.

Valuation should influence position sizing.

Quality tells me what to buy.

Valuation tells me when to buy.

My framework currently looks like this:

ZoneInterpretationBelow ₹850Strong Buy₹850–₹930Buy₹930–₹1,030Hold / WatchAbove ₹1,100Avoid aggressive additions

Below ₹850

At these levels, even relatively conservative valuation frameworks begin to show a meaningful margin of safety.

The investment case becomes less dependent on perfect execution and more dependent on simply avoiding major mistakes.

That is usually where I prefer to deploy capital.

₹850–₹930

The valuation starts tilting in my favor while still allowing room for execution risk.

The core franchise remains attractive and the optionality from investments is available at a more reasonable price.

₹930–₹1,030

This is approximately fair-value territory.

At these levels I would be comfortable holding existing positions but would not feel a strong urge to increase exposure.

Above ₹1,100

At these valuations, I would need a substantially more optimistic view regarding:

Core business growth

Margin expansion

The next generation of startup winners

Long-term value creation from the investment portfolio

Without that conviction, future returns become increasingly dependent on continued multiple expansion rather than fundamental value creation.

What Could Break My Thesis

No valuation is complete without understanding what can go wrong.

There are four developments that would make me materially less constructive on Info Edge.

1. Naukri Loses Pricing Power

Naukri remains the economic anchor of the entire group.

If recruiters begin reducing spend, switching platforms, or finding better alternatives, the valuation of the entire business changes.

The investment portfolio may be exciting, but the operating franchise pays the bills.

A weakening recruitment moat would force me to revisit almost every assumption in my model.

2. Adjacent Businesses Fail to Improve Economics

The long-term narrative depends on businesses such as 99acres and other operating segments continuing to improve efficiency and monetization.

If these businesses fail to progress toward stronger economics, some of the optionality embedded in my valuation disappears.

The result would be lower growth assumptions and reduced confidence in margin expansion.

3. Capital Allocation Discipline Deteriorates

One of the biggest strengths of Info Edge has been its investment discipline.

Successful startup investors often face a dangerous temptation after early wins.

Past success can encourage larger bets, weaker underwriting standards, or excessive optimism.

If management begins prioritizing valuation marks over governance and business quality, I would immediately apply a larger discount to the investment portfolio.

The track record has earned credibility.

But credibility must continually be re-earned.

4. A Prolonged Decline in Eternal or PB Fintech

The market currently recognizes Info Edge not only as an operating company but also as a successful allocator of capital.

If Eternal and PB Fintech experience significant and prolonged declines, investors may stop assigning value to that allocator identity.

In that scenario, the market could increasingly focus only on the operating business while assigning lower value to the investment portfolio.

That would compress valuation multiples even if the underlying businesses remain fundamentally sound.

The Bigger Lesson

One reason I enjoy studying Info Edge is that it demonstrates how valuation is often more about structure than forecasting.

Most investors spend their time debating whether revenue growth will be 12% or 15%.

In many situations, that is not where the real insight lies.

The real insight is understanding what exactly you are valuing.

Info Edge forces that discipline.

You cannot treat it as a simple internet stock.

You cannot treat it as a venture capital fund.

You cannot treat it as a holding company.

It is all three at the same time.

And that complexity creates both confusion and opportunity.

This is precisely the type of situation where Damodaran’s framework shines.

Separate the pieces.

Value each piece independently.

Then bring them back together.

Simple in principle.

Difficult in practice.

My Final Verdict

When I put everything together, I keep arriving at the same conclusion.

Info Edge is a high-quality business with:

A genuine moat

Meaningful promoter alignment

Strong free-cash-flow generation

Exceptional capital-allocation history

Significant optionality through its startup portfolio

Those are characteristics I actively seek in long-term compounders.

However, quality alone does not make something cheap.

At roughly ₹1,010 per share, I believe the market already recognizes much of what makes Info Edge special.

The Naukri franchise is appreciated.

The Eternal success story is appreciated.

The PB Fintech investment is appreciated.

A significant portion of the optionality is already reflected in the price.

That leaves me with a conclusion that may sound less exciting but is probably more useful:

Info Edge is not a deep-value opportunity today.

It is a high-quality business trading around intrinsic value.

Would I own it?

Yes.

Would I chase it aggressively?

Probably not.

Would I become significantly more interested if the market offered it closer to ₹850–₹900?

Absolutely.

If I were forced to summarize my view in a single sentence, it would be this:

Info Edge is one of the clearest examples in India of how Aswath Damodaran’s framework helps separate a great operating business from a great capital allocator living inside the same stock.

And that is precisely what makes it such a fascinating company to study.

Disclosure

This article is intended solely for educational and research purposes and should not be construed as investment advice. The valuation frameworks, assumptions, and conclusions presented here reflect my personal analysis and may prove incorrect. Investors should conduct their own due diligence and consider their risk tolerance before making any investment decisions.

https://aswathdamodaran.blogspot.com/2013/06/a-tangled-web-of-values-enterprise.html

DISCLAIMER

The content published in this post is intended solely for educational and informational purposes. I am not registered with SEBI as an investment advisor, research analyst, broker, or financial influencer, and nothing in this post should be construed as investment advice, stock recommendations, or solicitation to buy, sell, or hold any securities.

This analysis is part of my personal learning journey in finance and valuation, heavily influenced by academic frameworks and publicly available material from Aswath Damodaran, particularly his work on Cash, crossholdings, and others.

The post reflects my own interpretation and application of these concepts as a finance student and practitioner, and any errors or assumptions are entirely my own.The valuation models, assumptions, scenarios, and conclusions presented here are illustrative learning exercises, not predictions. They do not account for individual financial circumstances, risk tolerance, tax considerations, or investment objectives.

Readers are strongly encouraged to perform independent due diligence and/or consult a SEBI-registered financial professional before making any investment decisions. I shall not be responsible for any financial losses or outcomes resulting from reliance on this content.