Prof. Damodaran Framework in action - What HDFC Bank and Tata Motors Teach Us About Mergers and Demergers

DISCLAIMER: This article is part of my personal learning journey and is meant purely for educational and informational purposes. I have drawn insights from Prof. Aswath Damodaran’s publicly available teachings and financial information available in the public domain.

While preparing this write-up, I referred to platforms such as Screener and AI-based study tools to better understand the concepts and validate publicly available data such as company filings and information available for investors from the company domain. The interpretations and conclusions shared here are entirely my own, and any errors or misunderstandings are solely my responsibility.

This is not investment advice or a recommendation to buy, sell, or hold any securities. I encourage readers to do their own research and consult a SEBI-registered investment advisor before making any investment decisions.

The Synergy Paradox

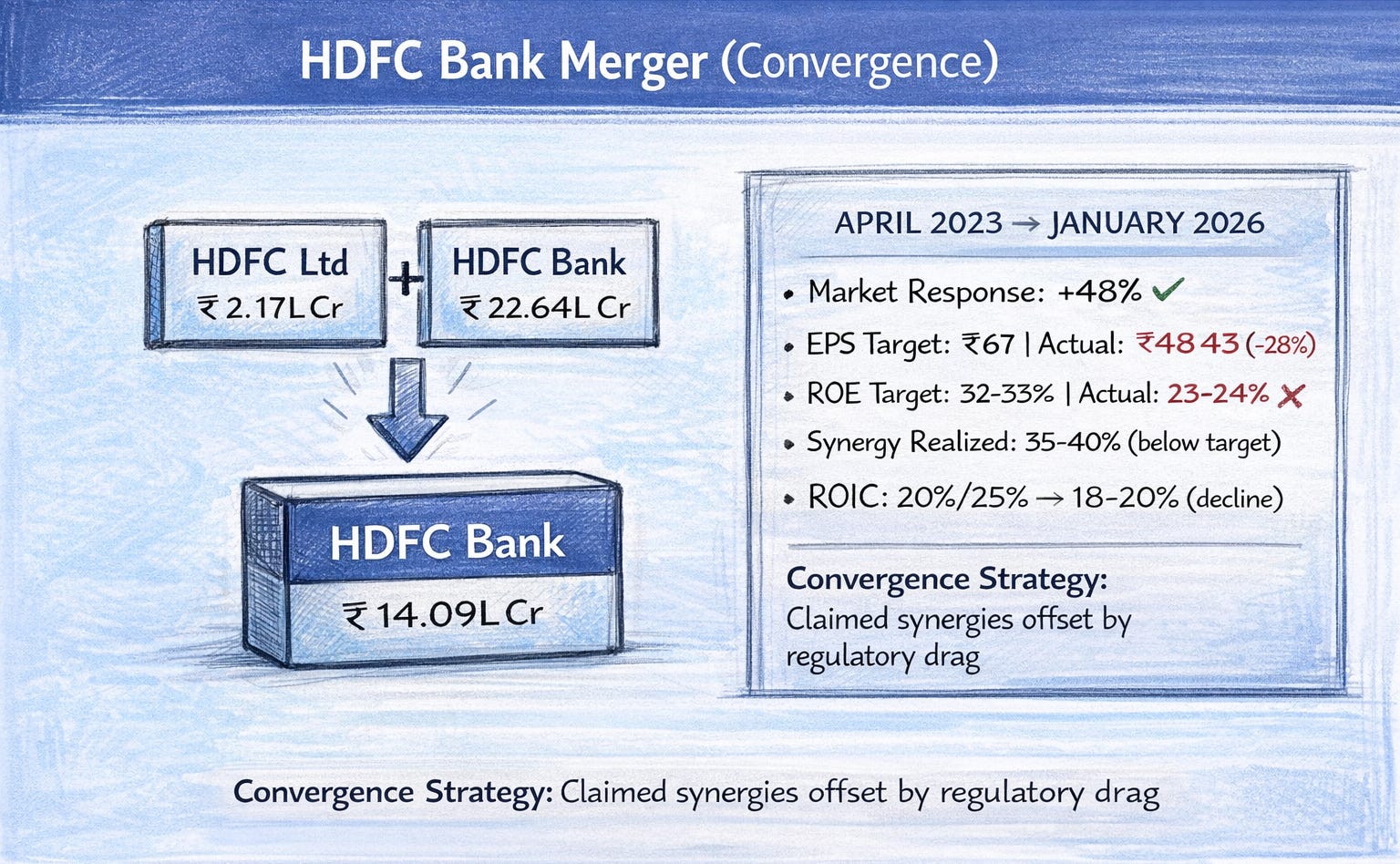

In April 2023, India witnessed it’s largest banking merger when HDFC Limited and HDFC Bank combined to create a financial behemoth with assets exceeding INR 17.87 lakh crore. The market cheered & stock prices surged, analysts projected massive synergies, and management promised transformational value creation.

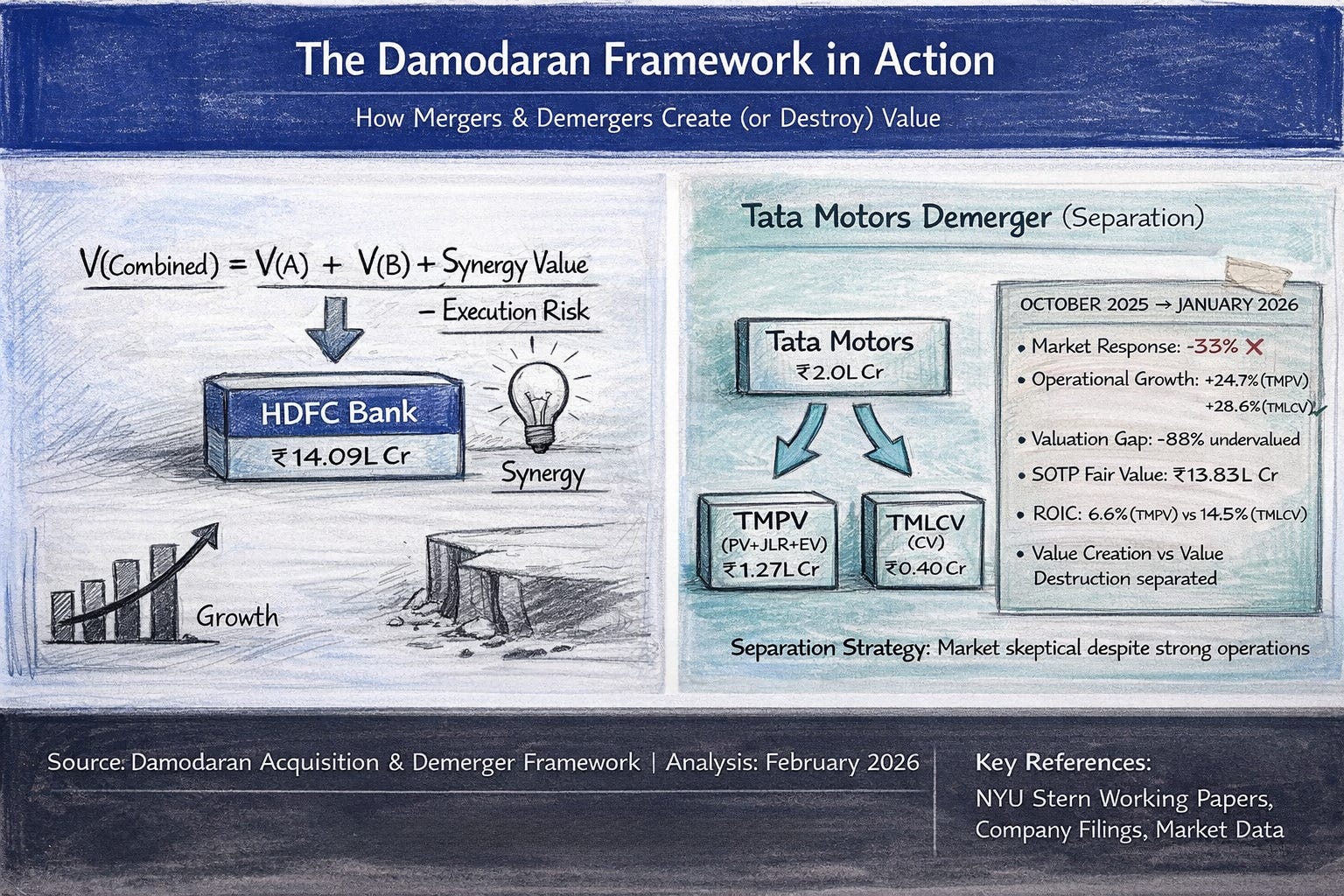

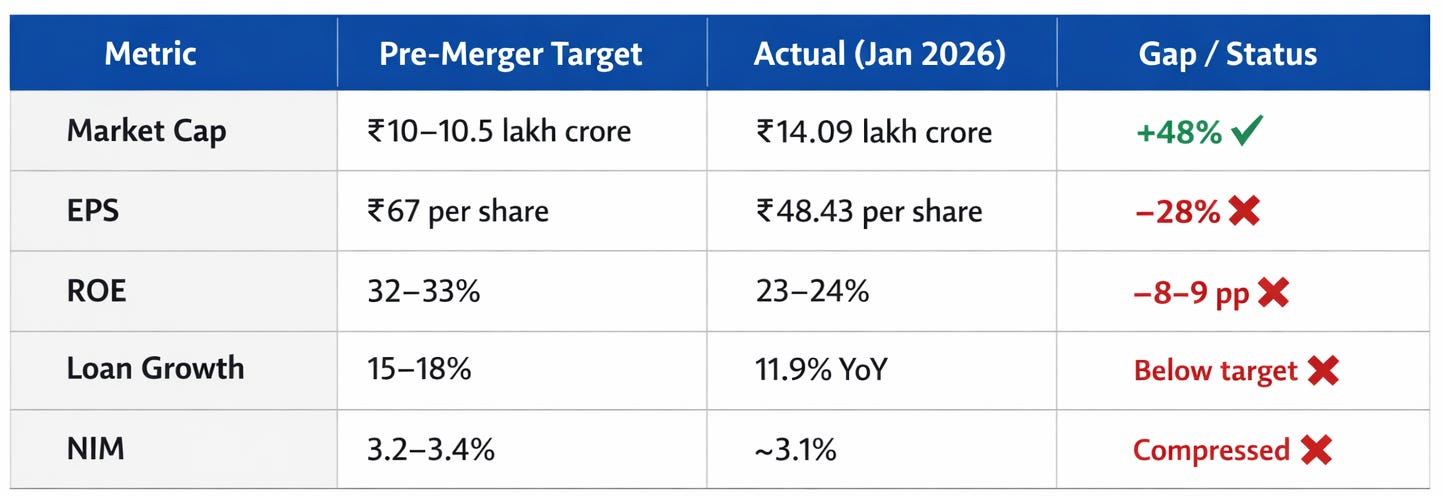

Fast forward to January 2026: The combined entity’s market cap has indeed grown by 48%, but synergies have materialized at only 35-40% of targets. EPS is 28% below projections, and ROE has contracted by 8-9 percentage points.

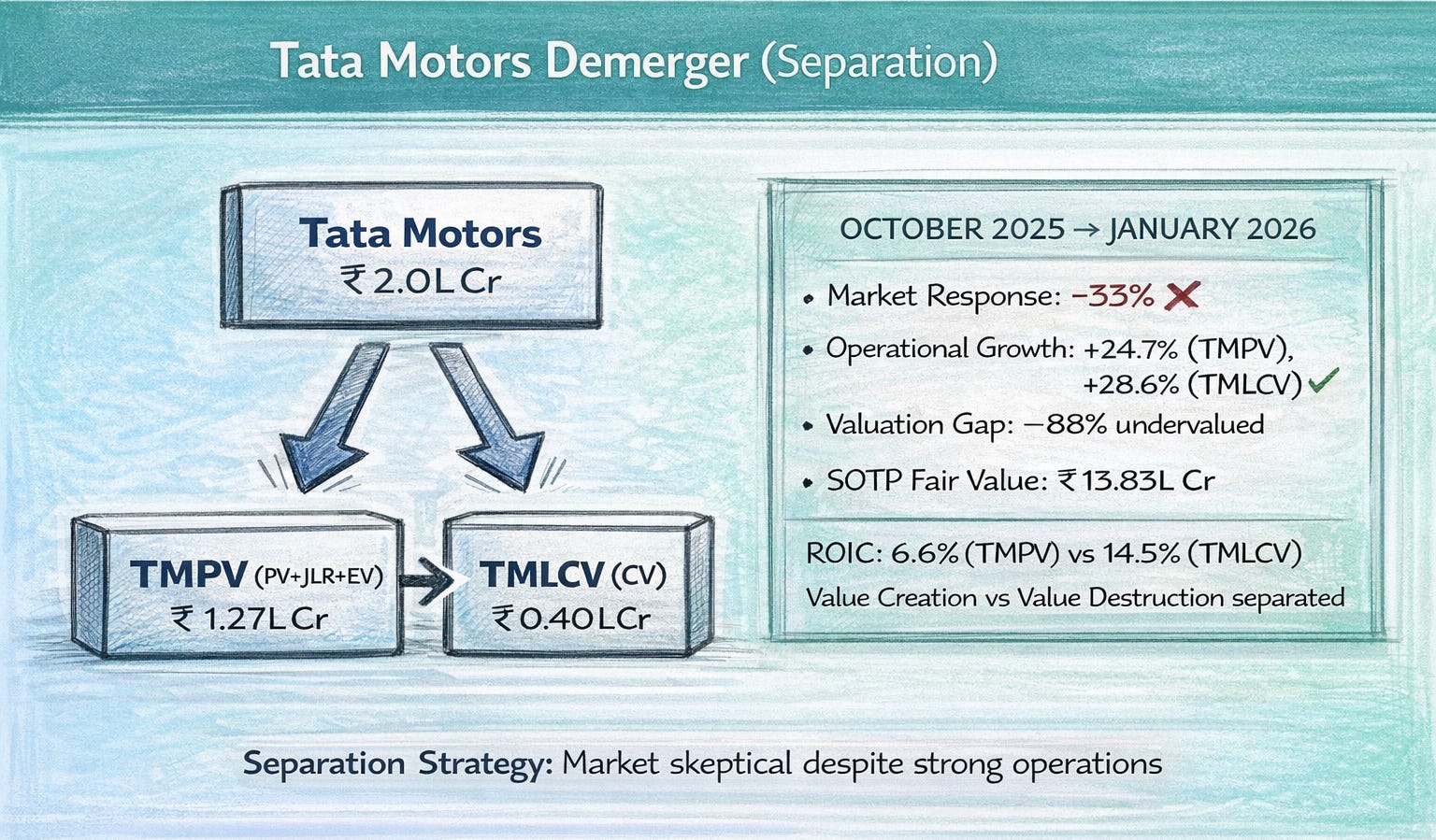

Meanwhile, in October 2025, Tata Motors executed the opposite strategy, splitting into two separate entities (passenger vehicles + JLR, and commercial vehicles). The market punished this decision with a 33% decline in combined market capitalization within three months, despite operational metrics showing +24.7% growth in passenger vehicles and +28.6% in commercial vehicles.

What explains these seemingly contradictory outcomes?

The answer lies in applying Aswath Damodaran’s acquisition and demerger valuation framework - a systematic approach that separates wishful thinking from rigorous value analysis. This article applies Damodaran’s methodology to both cases, revealing why synergy value is so difficult to capture in practice and what investors should watch for in corporate restructurings.

Understanding the Damodaran Framework

The Core Equation

Damodaran’s approach to valuing mergers and demergers rests on a deceptively simple foundation:

For Mergers:

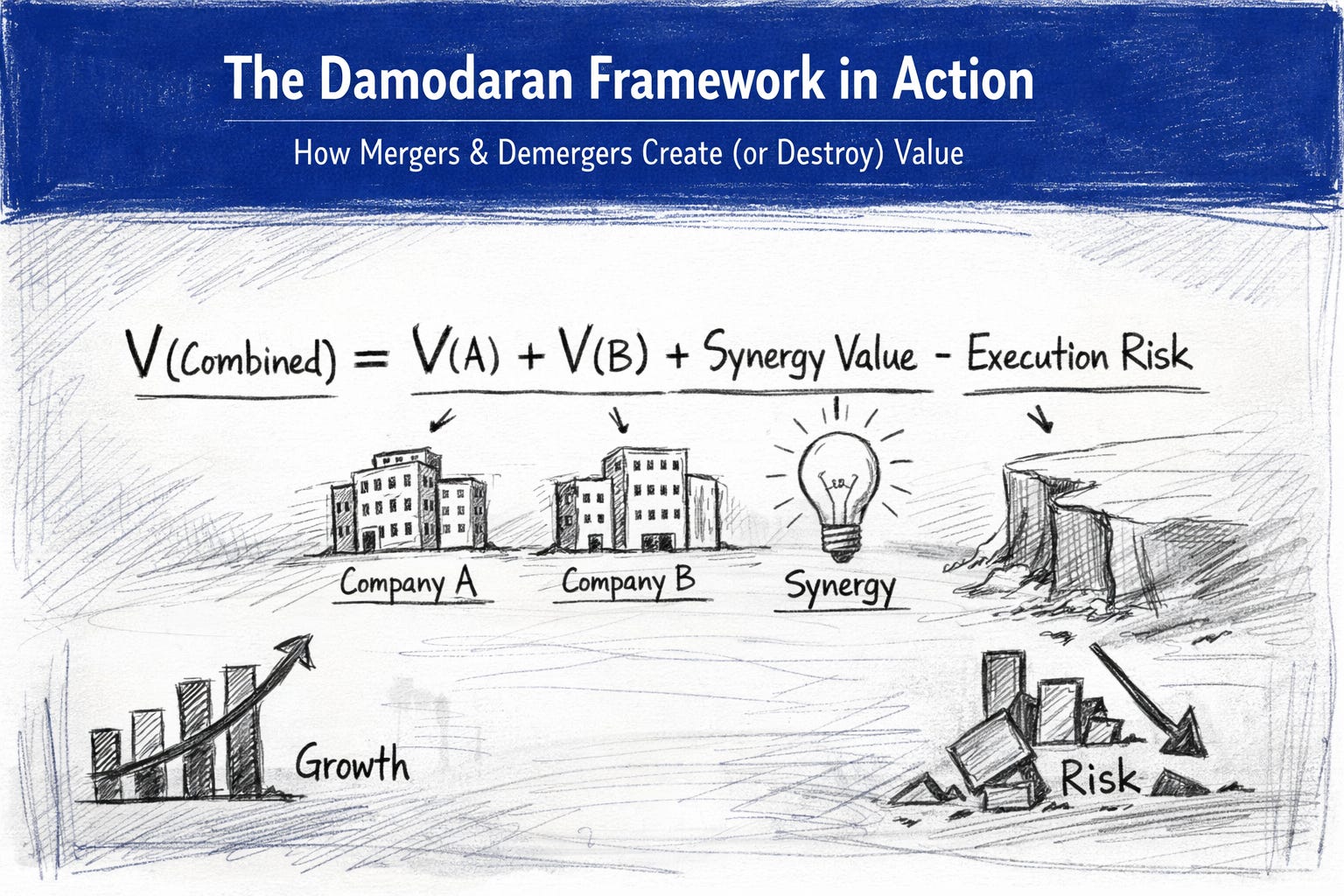

V(Combined) = V(A) + V(B) + Synergy Value - Execution Risk

For Demergers:

V(Parent) = V(Spun-off) + V(Remaining) + SOTP Premium - Separation Costs

As Damodaran writes in his seminal paper “The Value of Synergy”: Synergy, to have an effect on value, has to influence one of the four inputs into the valuation process

higher cash flows from existing assets, higher expected growth rates, a longer growth period, or a lower cost of capital.

The Four Critical Components

1. Standalone Entity Valuations: Calculate DCF-based free cash flow to equity (FCFE) using business-specific assumptions

2. ROIC Analysis: Determine if the combined entity earns more than its weighted average cost of capital (WACC)

3. Synergy/Control Premium: Quantify operating, financial, and strategic value sources with specific timelines

4. Execution Risk: Assess probability of synergy realization based on integration complexity

The framework’s power lies in its brutal honesty:

If you can’t quantify synergy with specific mechanisms and timing, it probably doesn’t exist.

Case Study 1 - HDFC Bank Merger (When Convergence Disappoints)

The Deal at a Glance

Transaction Date: April 2023

Deal Structure: HDFC Limited merged into HDFC Bank (reverse merger)

Combined Assets: Rs 17.87 lakh crore

Strategic Thesis: Cross-selling opportunities (70% non-overlapping customers), lower cost of funds, capital efficiency

Market Initial Response: +48% appreciation over 2.75 years

Applying the Damodaran Framework: Step-by-Step Valuation

Step 1: Standalone Valuations

HDFC Limited (Pre-Merger):

Loan Book: Rs 6.2 lakh crore (79% individual mortgages)

Net Interest Margin: 2.26%

ROE: 17–18%

ROIC: 20%

DCF Assumptions: 18% growth, 10.5% cost of equity, 6% terminal growth

Standalone Fair Value: Rs 2.17 lakh crore

HDFC Bank (Pre-Merger):

Loan Book: Rs 4.50 lakh crore (diversified portfolio)

Net Interest Margin: 3.4%

ROE: 35%+

ROIC: 25%

DCF Assumptions: 18% growth, 9.5% cost of equity, 6% terminal growth

Standalone Fair Value: Rs 22.64 lakh crore

Combined Value (No Synergy): Rs 24.81 lakh crore

Step 2: Synergy Estimation

Following Damodaran’s methodology of identifying specific synergy mechanisms:

Operating Synergies:

Cross-selling: Expected Rs 15,000 crore annual value from activating 70% non-overlapping HDFC customers

Cost of Funds Reduction: HDFC’s 5.83% to 4.8% via CASA deposits = Rs 10,000–15,000 crore value

Economies of Scale: Minimal (both already lean) = Rs 2,000–4,000 crore

Financial Dissynergies (The Hidden Killer):

SLR Requirements: 22% of deposits in government securities = Rs 80,000 crore in low-yield assets

CRR Requirements: 4–6% in RBI deposits = negative carry

Priority Sector Lending: 40% in prescribed sectors (lower yields) = Rs 10,000–15,000 crore annual opportunity cost

Net Synergy Value: + Rs 2.19 lakh crore (but regulatory drag reduced realized value to Rs 0.10–0.15 lakh crore)

Fair Value (April 2023): Rs 9.63–9.85 lakh crore (market priced at Rs 9.50 lakh crore — fairly valued)

Step 3: Real-World Outcome (January 2026)

Current Status (2.75 Years Post-Merger):

Why the Gap? The Damodaran Diagnosis

Root Cause 1: Regulatory Dissynergies Exceeded Operating Synergies

As Damodaran emphasizes in his CFA Institute talk:

“The problem with synergy is that it is easier to compute on paper than to create in practice.” - The value of Synergy

HDFC Bank discovered that converting HDFC’s housing finance book into bank assets triggered:

Statutory Liquidity Ratio obligations locking Rs 80,000+ crore in low-yield government securities

Cash Reserve Ratio requirements creating negative carry

Priority Sector Lending mandates forcing 40% of loans into lower-yielding segments

Annual regulatory drag: Rs 10,000–15,000 crore — effectively wiping out cross-selling synergies.

Root Cause 2: Cross-Selling Execution Delay

Expected synergy of activating 5–6 crore HDFC mortgage customers for banking products has taken 2–3 years instead of the projected 12 months. Behavioral change is hard — customers do not automatically switch banks just because of a merger.

Root Cause 3: Conglomerate Discount Emerged

Pre-merger, HDFC traded at 25–30x P/E (mortgage premium) and HDFC Bank at 20–22x P/E (banking premium). Post-merger: 18.92x P/E. The market now values it as a diversified bank, not a focused housing finance powerhouse.

The Damodaran Framework Score: 7/10

What It Got Right:

Identified potential synergy sources (cross-selling, funding cost)

Quantified regulatory dissynergies (prescient warning)

Valued both entities independently first

What It Missed:

Underestimated timing of synergy realization (3–5 years versus 12 months)

Did not fully anticipate market valuation multiple compression

Regulatory environment changes were directionally correct but magnitude was underestimated

Case Study 2 - Tata Motors Demerger (When Separation Creates Opportunity)

The Deal at a Glance

Demerger Effective Date: October 2025 (3 months ago as of analysis)

New Entities:

TMPV (Tata Motors Passenger Vehicles): PV + JLR + EV

TMLCV (Tata Motors Commercial Vehicles): CV + Iveco integration

Strategic Thesis:

Unlock pure-play multiples, separate high-ROIC from low-ROIC businesses, and enable focused capital allocation.

Market Response:

33% decline in combined value despite 25% operational growth

Applying the Damodaran Framework: SOTP Valuation

Step 1: Pre-Demerger ROIC Analysis

This is where Damodaran’s framework shines. As he notes:

When ROIC < WACC in a conglomerate, separation can help if each entity improves ROIC through focus.

Pre-Demerger Combined Entity

TMPV Segment ROIC: 6.6% (below WACC of 8–9%) → Destroying value

TMLCV Segment ROIC: 14.5% (above WACC of 8%) → Creating value

Problem: Strong CV business subsidizing weak JLR/PV transition

Step 2: Standalone Valuations

TMPV (Passenger Vehicles + JLR + EV)

Revenue: Rs 4.26 lakh crore (FY2025)

Current ROIC: 6.6% (JLR drag from cyberattack)

Normalized ROIC: 10–12% (post-JLR recovery by 2027–28)

DCF Assumptions: 10% growth, 10% cost of equity, 5% terminal growth

Standalone Fair Value: Rs 5.83 lakh crore

TMLCV (Commercial Vehicles)

Revenue: Approximately Rs 2.2 lakh crore

Current ROIC: 14.5%

Sustainable ROIC: 16–18% (post-Iveco integration)

DCF Assumptions: 14% growth, 9.5% cost of equity, 6% terminal growth

Standalone Fair Value: Rs 7.75 lakh crore

Combined Sum-of-Parts: Rs 13.58 lakh crore

Step 3: Separation Premium and Dissynergies

Separation Premium Sources

For TMPV:

Focused capital allocation for EV: + Rs 0.10–0.15 lakh crore

Luxury/EV multiple re-rating (18–20x vs 14–16x blended): + Rs 0.08–0.12 lakh crore

Management focus: + Rs 0.05–0.08 lakh crore

Total TMPV Premium: + Rs 0.35 lakh crore

For TMLCV:

Pure-play CV investor base (higher multiples): + Rs 0.05–0.08 lakh crore

Iveco integration value: + Rs 0.08–0.12 lakh crore

Dividend capacity unlocked: + Rs 0.03–0.05 lakh crore

Total TMLCV Premium: + Rs 0.30 lakh crore

Separation Costs

One-time costs: - Rs 0.02–0.03 lakh crore

Lost economies of scale: - Rs 0.03–0.05 lakh crore

Duplicate corporate overhead: - Rs 0.02–0.04 lakh crore

Lost cross-funding flexibility: - Rs 0.01–0.02 lakh crore

Total Dissynergies: - Rs 0.12–0.20 lakh crore

Fair Value Post-Demerger

TMPV: Rs 5.98 lakh crore (Rs 420–450 per share)

TMLCV: Rs 7.85 lakh crore (Rs 440–480 per share)

Combined SOTP: Rs 13.83 lakh crore

Current Market Cap (Jan 2026): Rs 1.67 lakh crore

Valuation Gap: 88% undervaluation

Step 4: Why the Market Is Wrong (Or Is It?)

Operational Reality (January 2026)

TMPV Production: +21.71% YoY (Q3 FY26)

TMPV Domestic Sales: +24.73% YoY

TMLCV CV Volumes: +28.6% YoY (November 2025)

Yet the market has hammered both stocks. Why?

Market Concern 1: JLR Cyberattack Overhang

In September 2025, JLR suffered a massive cyberattack that disrupted production. Phased restart only began in Q1 FY26. Market is pricing in a 50% probability that JLR recovery will be delayed or incomplete, which would reduce TMPV fair value by Rs 0.15–0.20 lakh crore.

Market Concern 2: CV Cycle Peak Fears

November 2025 CV growth of +28.6% looks like a cyclical peak. Commercial vehicle demand is inherently cyclical (4–5 year cycles). If the cycle turns in FY26–27, TMLCV fair value drops Rs 0.20–0.30 lakh crore.

Market Concern 3: Iveco Integration Risk

Tata Motors acquired Iveco’s bus and truck business for international expansion. Cross-border integrations have a 40–60% failure rate. Market is applying a 50–60% haircut to the estimated Rs 0.08–0.12 lakh crore Iveco synergies.

Market Concern 4: Investor Adjustment Period

Institutional investors need 3–6 months to rebalance portfolios after demergers. This creates temporary selling pressure and a 10–15% psychological discount.

The Damodaran Framework Score: 9/10

What It Got Right

Clearly separated value creation (ROIC > WACC) from value destruction (ROIC < WACC)

Quantified SOTP accurately using independent DCF models

Identified market timing risk

What It Struggled With

Difficult to quantify black swan events (JLR cyberattack one month before demerger)

Investor sentiment swings in a 3-month window are hard to model

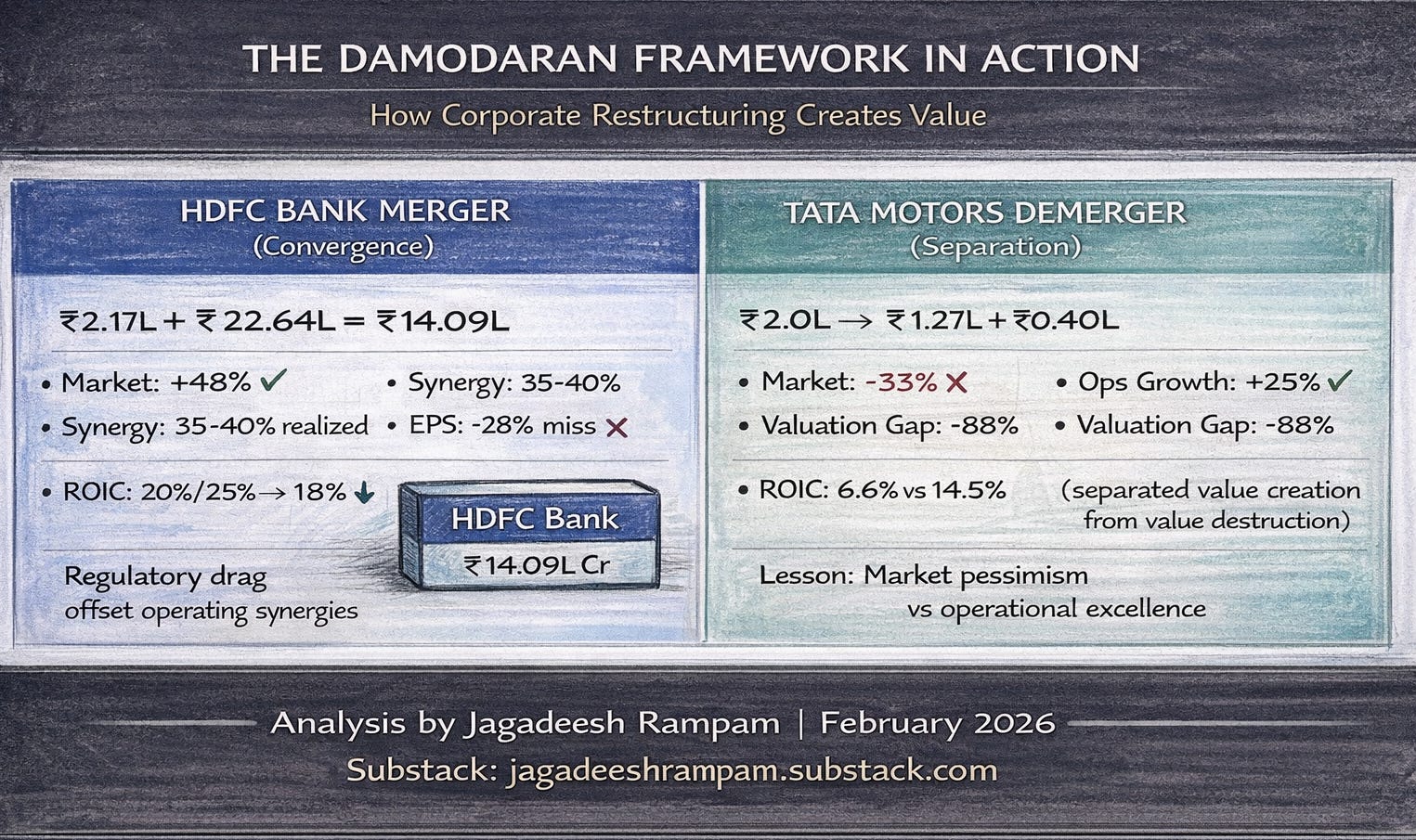

The Comparative Analysis

Synergy Quality Greater Than Synergy Quantity

As Damodaran emphasizes in his blog “Winning at a Loser’s Game”:

“The problem with acquisitions is not that synergy does not exist. The problem is that it is much more difficult to create synergy than to talk about it.”

HDFC Bank’s Lesson:

Claimed Rs 0.40–0.60 lakh crore in synergies, realized Rs 0.10–0.15 lakh crore (25–40% realization rate). Why? Regulatory dissynergies offset operating synergies — a classic case where financial engineering assumptions failed to account for regulatory realities.

Tata Motors’ Lesson:

Expected Rs 0.54–0.86 lakh crore separation premium. Realization at 0% after 3 months, but operational metrics show the strategy is working (+25% growth). The market is timing-pessimistic but fundamentally wrong about value.

When Mergers Make Sense (Damodaran’s Four Tests)

Drawing from Damodaran’s acquisition framework, mergers create value when:

Operating Synergy Test: Combined entity achieves lower costs or higher growth than sum of parts

HDFC Bank: Passed on paper, failed in execution (regulatory offset)

ROIC Improvement Test: Combined ROIC greater than standalone ROIC

HDFC Bank: Failed (20% + 25% resulted in 18–20% combined)

Financial Synergy Test: Cheaper capital or better use of cash

HDFC Bank: Partial pass (lower cost of funds, but SLR/CRR drag)

Control Premium Test: Better management creates value

HDFC Bank: Not applicable (both already optimally managed)

Verdict: The HDFC Bank merger made strategic sense, but execution complexity and the regulatory environment undermined value creation.

When Demergers Make Sense (The ROIC Separation Principle)

Demergers unlock value when:

ROIC Divergence Test: Businesses have radically different ROIC profiles

Tata Motors: Strong pass (6.6% vs 14.5% = 8 percentage point gap)

Capital Structure Test: Businesses need different leverage or capital allocation

Tata Motors: Passed (TMPV needs growth capital for EV, TMLCV can return cash via dividends)

Multiple Re-rating Test: Pure-play entities command higher multiples

Tata Motors: Expected (luxury 18–20x, CV 14–15x vs blended 14x), but market has not recognized yet

Focus and Execution Test: Separate management improves operational performance

Tata Motors: Validated (+25% operational growth post-separation)

Verdict: The Tata Motors demerger is fundamentally sound but market timing was unfortunate (JLR cyberattack one month before execution).

Investment Implications and Recommendations

HDFC Bank: The Fairly Valued (Hold)

Current Valuation (February 2026):

Price: Rs 915.80

P/E: 18.92x (vs sector 16.35x)

P/B: 2.65x

Fair Value Range: Rs 1,000–1,100

Upside: +3.7% to +9.2%

Investment Thesis:

Stock has re-rated from merger euphoria (48% gain) to fundamental value

Synergies are slowly materializing but the 3–5 year timeline remains

Regulatory environment stable but unlikely to improve materially

Growth trajectory reset to 11–12% (from 18%+ pre-merger)

Recommendation: HOLD for long-term investors (5+ years)

Catalyst Watch: Q4 FY26 guidance (March 2026) for CASA deposit trends

Risk: Growth remains structurally stuck at 11–12% (not temporary)

Positioning: Core holding for dividend income (1.2% yield growing 15–18%) plus steady 8–10% capital appreciation

Tata Motors: The Mispriced Demerger Opportunity

TMPV (Passenger Vehicles + JLR + EV)

Current Price: Approximately Rs 375.70

Fair Value: Rs 420–450 (12-month target)

Upside: +20–28%

Bull Case (JLR recovery plus EV ramp): Rs 520–580 (+48–65%)

TMLCV (Commercial Vehicles)

Current Price: Approximately Rs 403

Fair Value: Rs 440–480 (12-month target)

Upside: +9–19%

Bull Case (Iveco success plus cycle extension): Rs 520–580 (+29–44%)

Investment Thesis:

Market is pricing in excessive pessimism on JLR (50% probability of failure)

CV cycle fears appear overdone — structural demand from infrastructure and logistics remains strong

Operational metrics (+25% growth) validate the demerger strategy

SOTP discount of -33% appears irrational given fundamentals

Recommendation:

TMPV: BUY on dips below Rs 330 (high-risk, high-reward; binary outcome based on JLR)

TMLCV: ACCUMULATE for dividend yield and value (lower risk, steady returns)

Portfolio Strategy: 60% TMPV / 40% TMLCV for optimal risk-adjusted returns

Key Catalysts:

TMPV: Q4 FY26 results (May 2026) showing JLR recovery trajectory

TMLCV: Q3 FY26 guidance (January 2026) on Iveco integration progress

Timeline to Value Realization: 12–24 months (much faster than HDFC Bank’s 3–5 years)

What Damodaran’s Framework Teaches Us

The Three Meta-Lessons

Lesson 1: Synergy Is a Story, Valuation Is a Number

As Damodaran writes:

“Synergy is so seldom delivered in acquisitions because it is incorrectly valued, inadequately planned for and much more difficult to create in practice than it is to compute on paper.”

HDFC Bank claimed Rs 0.40–0.60 lakh crore in synergies. The framework forced discipline: “Show me the mechanism. Show me the timing. Show me the probability.”

Result: Only Rs 0.10–0.15 lakh crore was truly defensible.

Lesson 2: ROIC Is the North Star

The single most powerful diagnostic in both cases was ROIC analysis:

HDFC Bank: Combined ROIC decline (20% and 25% down to 18%) signaled value destruction risk

Tata Motors: ROIC divergence (6.6% vs 14.5%) clearly indicated the businesses should be separated

If ROIC does not improve materially, the restructuring is financial engineering, not value creation.

Lesson 3: Markets Eventually Recognize Value, But Timing Is Everything

HDFC Bank: Market ignored synergy shortfalls for more than 2 years due to sector tailwinds

Tata Motors: Market focused on short-term fears (JLR, CV cycle) despite operational strength

For investors: Damodaran’s framework identifies intrinsic value, but realizing that value requires patience and catalysts.

When to Use This Framework

Optimal Use Cases

Mega-mergers where synergies are the deal’s core value proposition (HDFC Bank)

Conglomerate demergers where ROIC profiles diverge strongly (Tata Motors)

Control changes where operational improvements are promised

Financial engineering deals involving capital structure optimization

Limitations

Difficulty quantifying execution risk (50%? 70%? Hard to know precisely)

Regulatory environment changes are difficult to model (for example, SLR and CRR surprises)

Market sentiment can override fundamentals for 6–12 months (Tata Motors post-demerger)

Black swan events (such as the JLR cyberattack) are inherently unpredictable

Damodaran’s framework is necessary but not sufficient. Combine it with(My 2 cents):

Market sentiment analysis (VIX, sector rotation, institutional flows)

Industry and cycle analysis (CV cycle position, mortgage market health)

Regulatory horizon scanning (anticipating policy changes)

Management track record assessment (integration and execution capability)

Conclusion: The Paradox of Value Creation

The HDFC Bank merger and Tata Motors demerger present a fascinating paradox:

HDFC Bank: Combined entities with strong standalone performance resulted in less value creation than expected, yet the market still rewarded it (+48%).

Tata Motors: Separated value-destroying from value-creating businesses, operational metrics validated the strategy, yet the market punished it (-33%).

Damodaran’s framework explains both outcomes:

For HDFC Bank: Synergy was overestimated because regulatory dissynergies were not fully anticipated. The market’s +48% gain reflects sector multiple expansion, not merger synergies — a key distinction the framework helps clarify.

For Tata Motors: The SOTP valuation is clear (Rs 13.83 lakh crore fair value vs Rs 1.67 lakh crore market cap). The -33% gap reflects timing and sentiment, not fundamentals. The framework identifies this as a temporary mispricing.

The Final Verdict

Damodaran’s acquisition and demerger framework is the most rigorous tool for separating value creation from value destruction in corporate restructurings.

But as Damodaran himself cautions:

“The problem is not with the valuation. The problem is with human nature — we want to believe in synergy, even when the numbers do not support it.”

For Investors

Use the framework to value restructurings independently

Identify where market price diverges from intrinsic value

Have the patience to wait for catalysts (HDFC: 3–5 years, Tata: 12–24 months)

Recognize when markets are temporarily wrong (Tata Motors today) versus when fundamentals disappoint (HDFC Bank’s synergy shortfall)

The best corporate restructurings are not the ones with the biggest synergy claims — they are the ones where ROIC improves materially and management can clearly demonstrate how.

Appendix: Key Metrics at a Glance

HDFC Bank (February 2026)

Price: Rs 915.80 | Fair Value: Rs 1,000–1,100 | Upside: +3.7% to +9.2%

P/E: 18.92x | P/B: 2.65x | ROE: 23–24% | Loan Growth: 11.9%

What I’m doing: HOLD | Time Horizon: 3–5 years

TMPV (February 2026)

Price: Approximately Rs 350 | Fair Value: Rs 420–450 | Upside: +20–28%

P/E: 1.53x (distorted) | P/B: 1.20x | ROE: 9.95%

What I’m doing: BUY on dips | Time Horizon: 12–18 months

TMLCV (February 2026)

Price: Approximately Rs 403 | Fair Value: Rs 440–480 | Upside: +9–19%

EV/EBITDA: 4.47x | ROE: 23.96% | CV Growth: +28.6%

What I’m doing: ACCUMULATE | Time Horizon: 18–24 months

References and Further Reading

[1] HDFC Bank Q3 FY26 Results (January 2026). HDFC Bank reports first double-digit loan growth post-merger at 11.9% YoY. Economic Times, January 2026.

[2] Tata Motors Demerger Impact Report (October 2025). TMLCV CV volumes surge +28.6% in November 2025. Business Standard, October 2025.

[3] Damodaran, A. (2005). The Value of Synergy. Stern School of Business Working Paper.

Available at: https://pages.stern.nyu.edu/~adamodar/pdfiles/papers/synergy.pdf

[4] Damodaran, A. (2024). Acquisition Valuation. NYU Stern Teaching Materials.

Available at: https://pages.stern.nyu.edu/~adamodar/pdfiles/AcqValn.pdf

[5] Manickaraj, M. and Roy, A. (2023). The Merger of HDFC Limited with HDFC Bank: Synergy or Concentration? NIBM Working Paper. Notes regulatory obligations (SLR 22%, CRR 4–6%, Priority Sector 40%) create Rs 10,000–15,000 crore annual drag.

[6] CFA Institute. (2019). Aswath Damodaran on Acquisitions: Just Say No. CFA Institute Blog, February 27, 2019.

Available at: https://blogs.cfainstitute.org/investor/2019/02/28/aswath-damodaran-on-acquisitions-just-say-no/

[7] HDFC Bank Annual Report FY2025. CEO Sashidhar Jagdishan notes cross-selling activation slower than expected, targeting completion by FY2027. HDFC Bank Investor Relations, July 2025.

[8] Damodaran, A. (2002). Investment Valuation: Tools and Techniques for Determining the Value of Any Asset (2nd edition). Wiley Finance. Chapter on demergers and spinoffs emphasizes ROIC improvement as primary value driver.

[9] Tata Motors Q3 FY26 Production Report. TMPV production volumes increase +21.71% YoY with domestic PV sales +24.73%. Tata Motors Press Release, January 2026.

[10] Tata Motors JLR Cyberattack Impact Analysis (September 2025). Phased restart announced for Q1 FY26 with full recovery expected post-holiday season February–March 2026. Reuters, October 2025.

[11] Damodaran, A. (2015). Winning at a Loser’s Game? Control, Synergy and the ABInBev-SABMiller Merger. Musings on Markets blog, October 22, 2015.

Available at: https://aswathdamodaran.blogspot.com/2015/10/winning-at-losers-game-control-synergy.html

[12] Damodaran, A. (2024). Valuing Synergy. NYU Stern Spring 2024 Session Materials.

Available at: https://pages.stern.nyu.edu/~adamodar/podcasts/valspr24/session25slides.pdf

[13] HDFC Bank Merger Analysis by Prime Investor (2024). Analysis - Impact of the HDFC merger and our recommendation. Prime Investor Research Report, July 5, 2024.

Available at: https://primeinvestor.in/reports/analysis-impact-of-hdfc-merger-our-recommendation/

About This Analysis

This analysis was prepared using Aswath Damodaran’s published valuation frameworks, publicly available financial statements, analyst reports, and market data as of February 17, 2026. All DCF calculations use standard corporate finance assumptions (WACC, terminal growth 5–6%, industry-standard reinvestment rates) and are based on Damodaran’s teaching materials from NYU Stern School of Business.

Disclaimer: This analysis is for educational and informational purposes only. It does not constitute investment advice. Readers should conduct their own due diligence and consult with financial advisors before making investment decisions. I have a vested interest in doing the analysis as I am long term holder of these stocks and would like to evaluate once in a half year for building conviction on holding or exiting or partial exit.

Changelog and Updates:

February 17, 2026: Initial publication with data through January 2026

Future updates will track Q4 FY26 results for both HDFC Bank and Tata Motors entities

DISCLAIMER

The content published in this post is intended solely for educational and informational purposes. I am not registered with SEBI as an investment advisor, research analyst, broker, or financial influencer, and nothing in this post should be construed as investment advice, stock recommendations, or solicitation to buy, sell, or hold any securities.

This analysis is part of my personal learning journey in finance and valuation, heavily influenced by academic frameworks and publicly available material from Aswath Damodaran, particularly his work on Synergies and valuation.

The post reflects my own interpretation and application of these concepts as a finance student and practitioner, and any errors or assumptions are entirely my own.The valuation models, assumptions, scenarios, and conclusions presented here are illustrative learning exercises, not predictions. They do not account for individual financial circumstances, risk tolerance, tax considerations, or investment objectives.

Readers are strongly encouraged to perform independent due diligence and/or consult a SEBI-registered financial professional before making any investment decisions. I shall not be responsible for any financial losses or outcomes resulting from reliance on this content.

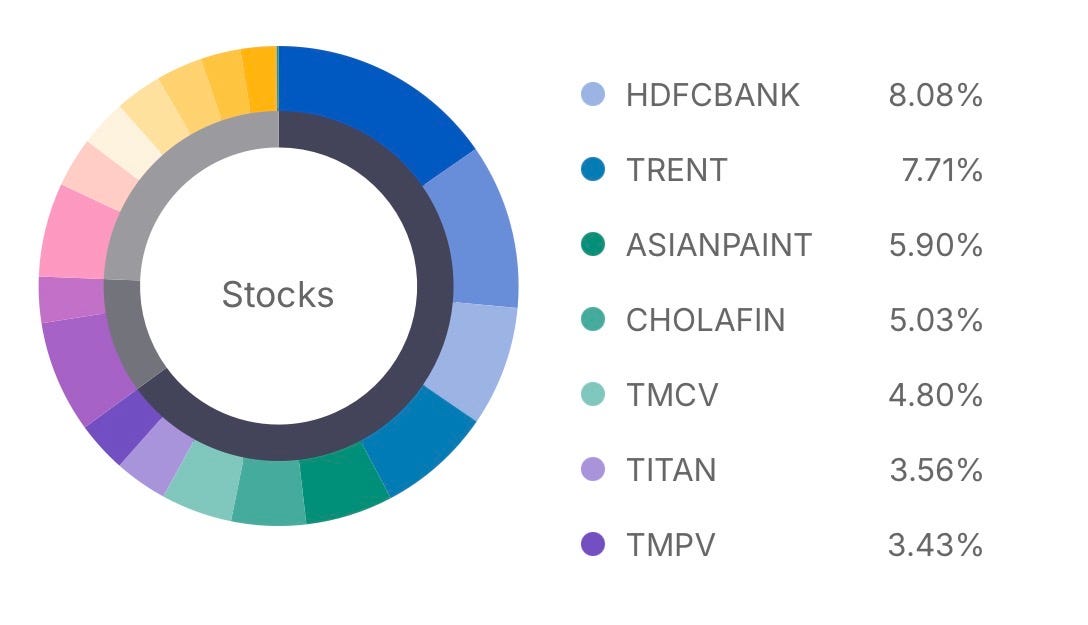

🔍 Holdings & Transparency Disclosure

Disclosure of Personal Holdings

Where applicable, I disclose my personal holdings in the discussed securities, including approximate portfolio allocation percentages and unrealized profit/loss as of the mentioned date, purely in the interest of transparency.

Such disclosure does not constitute a recommendation or endorsement. My positions may change at any time without notice, and I am under no obligation to update previous disclosures or analyses.

My personal holdings of HDFC Bank & Tata Motors(PV &CV) dated on 19th Feb 2026 (against overall Portfolio)